Eugen Soloviov

Trading-systems engineer

Trading-systems engineer building bots since 2017: cross-exchange arbitrage (connected up to 30 venues), cointegration-based pairs arbitrage across spot and futures, scalping, news and sentiment-driven strategies, trend algorithms, and portfolio management and balancing algorithms. Also builds sub-millisecond order execution, big-data warehouses, backtesting engines, AI agents, and trading interfaces (incl. open-source profitmaker.cc). Stack: JS/TS, Python, Rust/Zig/Go, DevOps, backend, frontend, architecture.

Articles

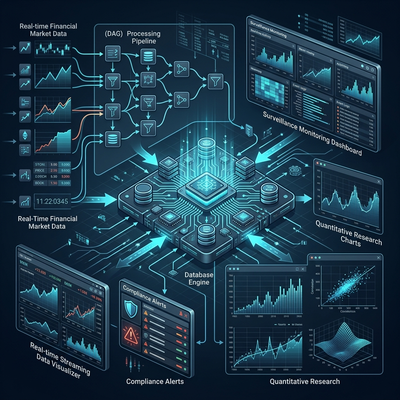

OneTick: The Platform Where Exchanges Catch Spoofers and Hedge Funds Hunt Alpha

Architecture of OneTick — an enterprise-grade time-series engine for tick data. DAG queries via Event Processors, unified real-time and historical data, market surveillance (MiFID II, MAR, SEC), TCA, quant research, and comparison with kdb+.

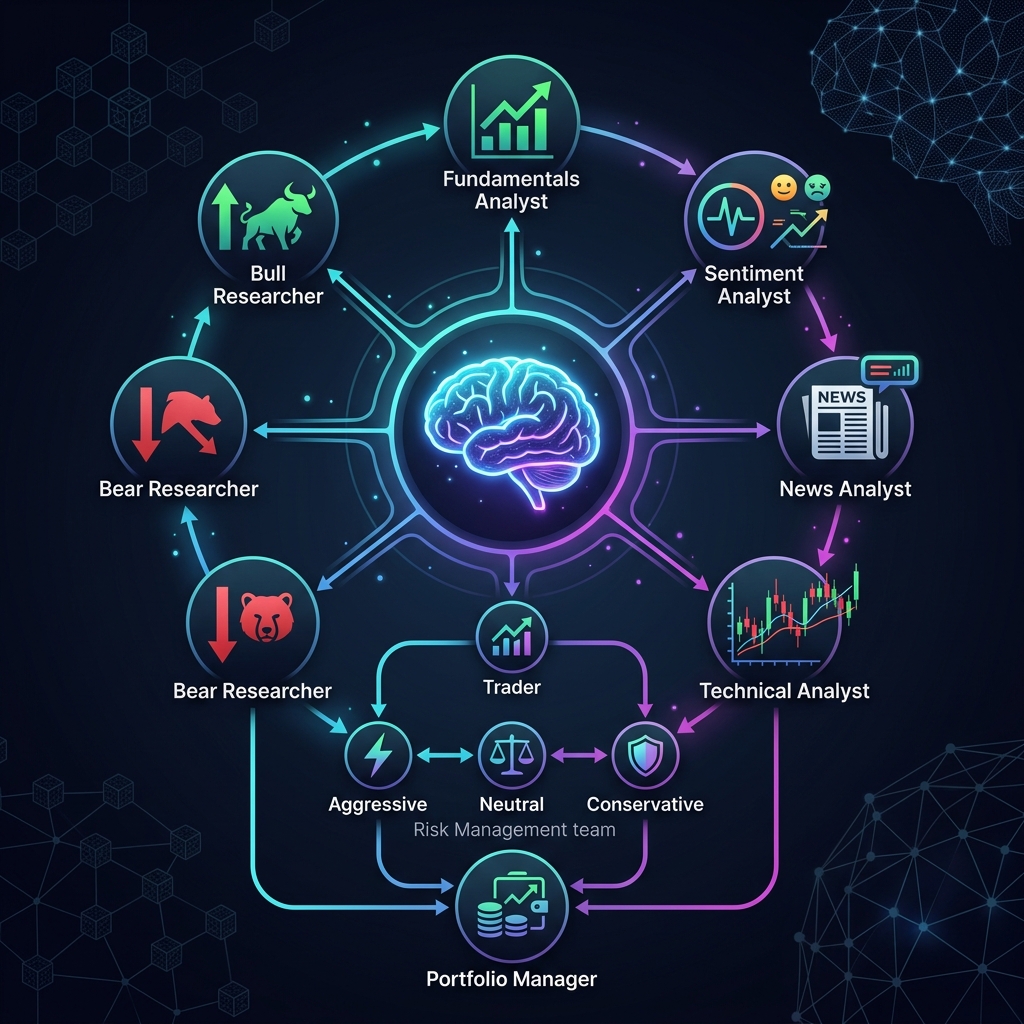

TradingAgents: Multi-Agent AI Framework That Models a Hedge Fund

Architecture deep dive into TradingAgents — an open-source LangGraph framework where LLM agents (analysts, researchers, trader, risk management, portfolio manager) engage in structured debates to make trading decisions.

Prediction Market Arbitrage: Hidden Costs, Fees, and the Real Math

Breaking down arbitrage between Polymarket, Limitless, Predict.fun, Opinion, and Kalshi. Dynamic fees, cross-chain bridges, slippage, resolution risk — and why a 5% spread may still lose money.

T-Bricks (Broadridge): How the Platform Powering Prop Firms Works

Architecture of T-Bricks — a modular HFT platform in C++ for market making, ETF arbitrage, and centralized risk management. 100+ clients, 150+ exchanges, nanosecond latencies.

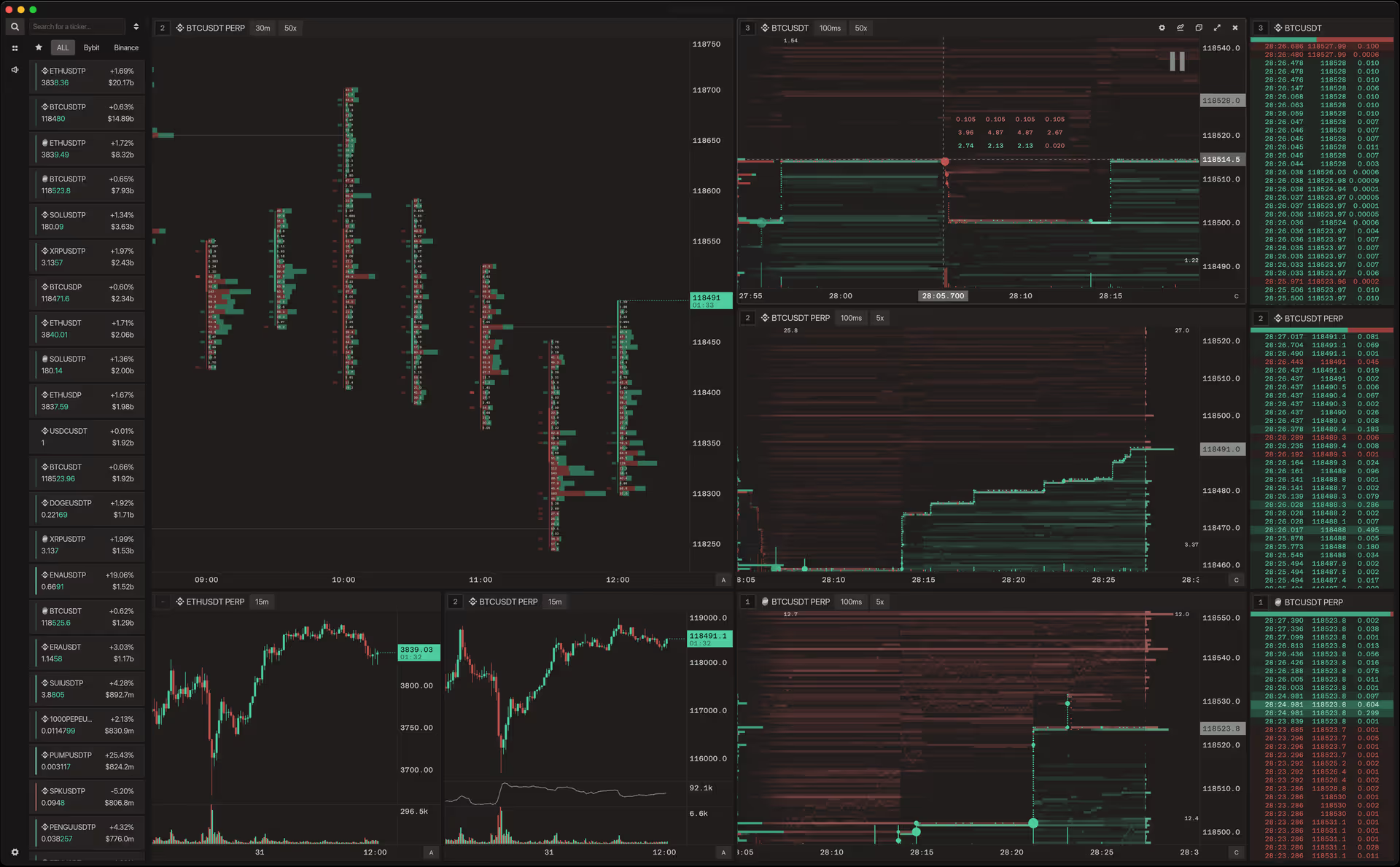

Flowsurface: Open-Source Orderflow Platform for Crypto Markets

A review of Flowsurface — a free desktop application built in Rust for real-time DOM heatmap, footprint charts, time & sales, and depth ladder visualization. Supports Binance, Bybit, Hyperliquid, OKX, and MEXC.

Fincept Terminal: Open-Source Bloomberg Terminal Alternative Built on C++ and AI

In-depth review of Fincept Terminal v4 — a native desktop application built on C++20 and Qt6 with 37 AI agents, QuantLib, and 100+ data connectors for professional trading.

Kronos: A Foundation Model That Teaches Candlestick Charts to Speak Transformer Language

Review of Kronos — a foundation model for OHLCV candle forecasting. BSQ tokenizer, hierarchical decoder, two-stage sampling, Qlib training pipeline. How a model learns the 'language' of the exchange.

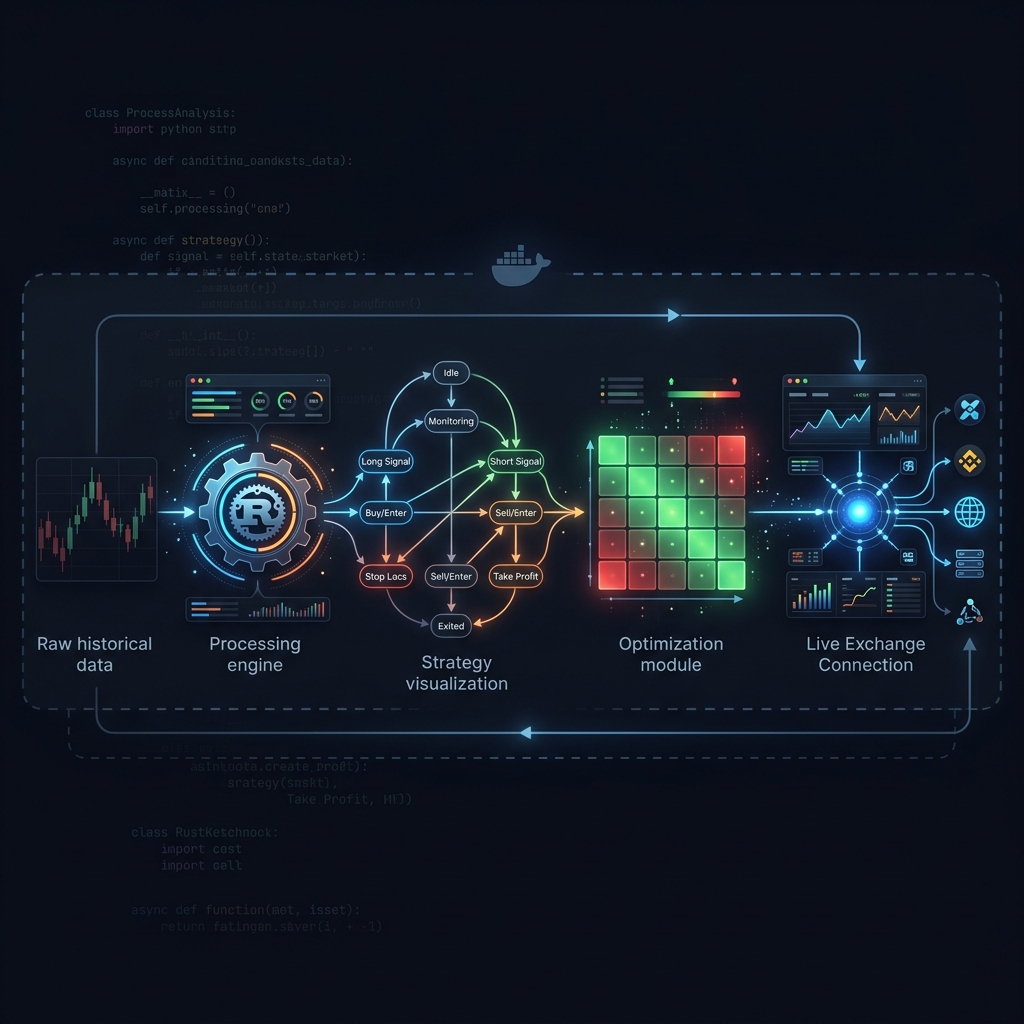

Jesse: Crypto Algo-Trading Framework with a Minute-Based Engine in Python and Rust

In-depth review of Jesse — an algo-trading framework for crypto markets. Minute-based simulation, strategies as state machines, Rust-accelerated indicators, optimization with overfitting protection, and the boundary between open-source core and live trading.

AI Hedge Fund: A Multi-Agent Fund Where AI Analysts Vote on Trades

A deep dive into AI Hedge Fund by virattt — an open-source system where multiple LLM agents with different analysis styles build a portfolio through a risk filter. Architecture, agents, limitations, and lessons for real systems.

AI4Finance Foundation: The FinGPT, FinRL, and FinRobot Ecosystem for Algo-Trading

Complete guide to the AI4Finance Foundation ecosystem: FinGPT (LLM + LoRA for finance), FinRL (reinforcement learning for trading), FinRobot (multi-agent orchestration). Satellites, pipelines, and practical usage.

VectorBT: The Fastest Backtesting Framework for Python

Overview of VectorBT — an innovative quantitative analysis library that changes the approach to backtesting thanks to the power of NumPy and Numba.

Copula Models for Joint Risk Modeling in Crypto Portfolios

Beyond linear correlation — using copula models to capture tail dependence and joint risk in cryptocurrency portfolios for accurate VaR and CVaR estimation.