O critério de Kelly para estratégias: como dimensionar posições e alocar capital

Uma estratégia com valor esperado positivo ainda pode destruir sua conta se o tamanho da aposta estiver errado. Percorremos o critério de Kelly desde a dedução da fórmula até uma carteira de estratégias: por que o Kelly completo é perigoso, como o Kelly fracionário captura 75% do crescimento com metade da volatilidade, e qual receita de dimensionamento você deveria realmente aplicar no trading algorítmico. No meio do artigo há uma calculadora interativa que mostra como a fração de Kelly move o retorno e o risco.

A pergunta que toda estratégia é obrigada a responder

Você tem uma estratégia com edge positivo: no longo prazo, ela gera dinheiro. Resta um detalhe — qual fração do capital colocar em uma única operação ou alocar a uma única estratégia.

Esta não é uma questão secundária, mas a central. O valor esperado positivo não salva você da ruína: aposte demais, e uma sequência de perdas leva sua conta a uma zona da qual não há recuperação estatística (veja A assimetria entre perdas e ganhos). Aposte de menos, e você deixa a maior parte do crescimento potencial na mesa.

O critério de Kelly dá uma resposta precisa: é a fração de capital que maximiza a taxa de crescimento de longo prazo — a geométrica, não a aritmética. É o crescimento geométrico que determina onde sua conta termina depois de mil operações, porque os retornos se multiplicam em vez de se somarem (veja A natureza multiplicativa dos retornos).

De onde vem a fórmula: maximizar o logaritmo do capital

A ideia central de Kelly (1956) e, mais tarde, de Thorp: o que você deve otimizar não é o lucro esperado de uma única operação, mas o logaritmo esperado do seu capital final. O logaritmo não aparece por acaso — é a única função cuja maximização faz o capital crescer na taxa geométrica máxima.

O caso binário: uma aposta com dois resultados

Suponha que, com probabilidade , a aposta retorna um pagamento líquido de por unidade (as odds), e que, com probabilidade , perdemos a própria aposta. Apostamos uma fração do nosso capital. Após uma operação, o capital é multiplicado por em caso de vitória e por em caso de derrota.

Crescimento logarítmico esperado:

Tomamos a derivada em relação a e igualamos a zero:

A solução é a fórmula de Kelly:

Em palavras: a fração ótima é igual ao seu edge dividido pelas odds. Sem edge () — sem aposta.

Exemplo

Uma estratégia vence 55% das operações com uma relação de pagamento de 1:1 ():

O Kelly completo indica arriscar 10% do capital por operação. Guarde esse número — mais adiante veremos por que quase ninguém deveria apostar exatamente essa quantia.

O caso contínuo: retornos em vez de apostas

No trading, uma operação raramente se parece com uma aposta de dois resultados — há uma distribuição de retornos. Para retornos com média e variância por período, o crescimento logarítmico esperado com alavancagem (fração) é aproximadamente:

O máximo é atingido em:

Esta é a famosa forma contínua de Kelly (também conhecida como fração de Merton). E a taxa de crescimento no ótimo está ligada ao índice de Sharpe de forma notavelmente elegante:

Uma conclusão digna de ser fixada na parede: a taxa máxima de crescimento geométrico de uma carteira é igual à metade do quadrado do seu Sharpe. Dobre o Sharpe e você quadruplica a taxa de crescimento do capital.

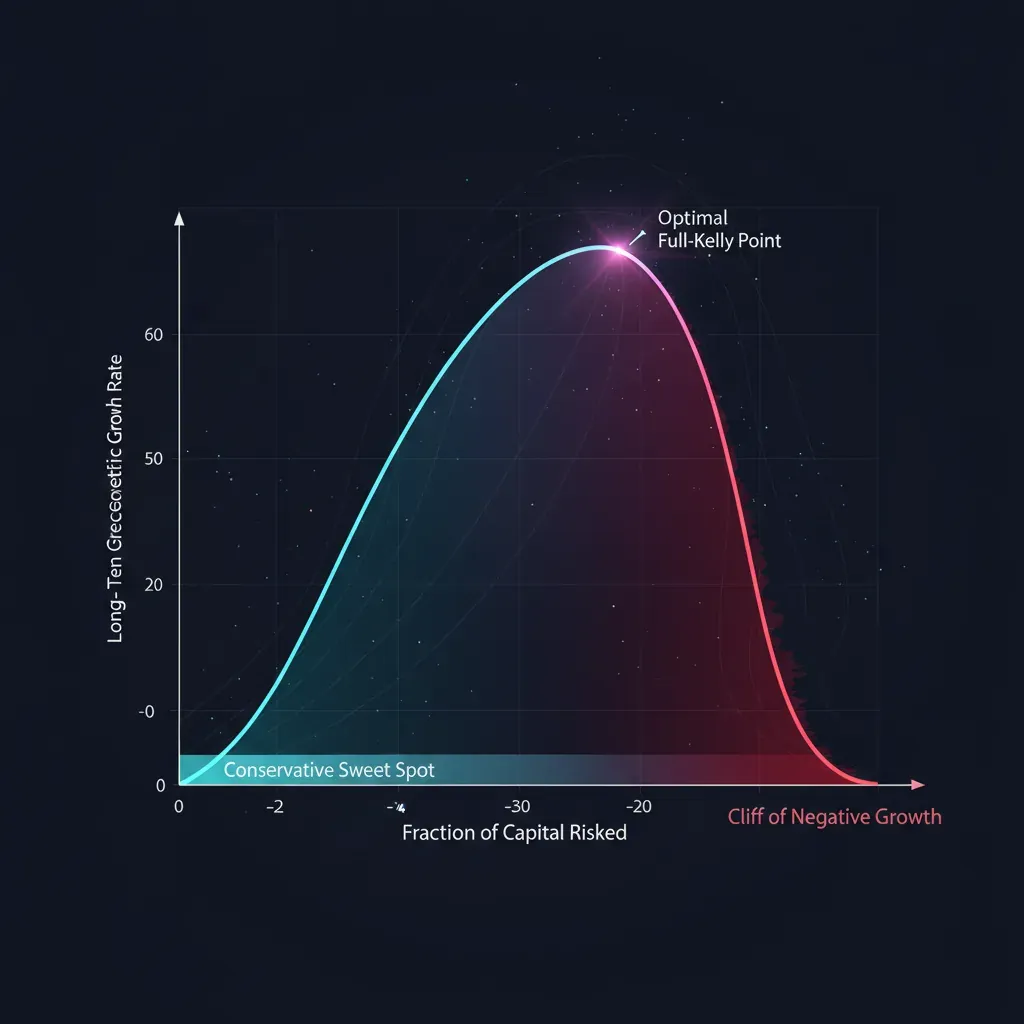

Por que o Kelly completo é demais

A fórmula dá o ótimo matemático para o crescimento. Mas esse ótimo tem um preço sobre o qual a fórmula se cala: uma volatilidade de trajetória monstruosa e drawdowns que quebram qualquer conta real e qualquer pessoa real.

A geometria de se afastar do ótimo

Substitua a fração (onde é o multiplicador de Kelly: é o Kelly completo, é o meio Kelly) na fórmula de crescimento. Em relação ao máximo, obtemos:

Esta parábola conta toda a história da gestão de risco em uma única linha:

| Multiplicador | Fração do crescimento | Volatilidade | Comentário |

|---|---|---|---|

| 0.25 (um quarto) | 43.8% | 25% | quase metade do crescimento com um quarto do risco |

| 0.50 (metade) | 75.0% | 50% | o ponto ideal dos profissionais |

| 1.00 (completo) | 100.0% | 100% | crescimento máximo, volatilidade selvagem |

| 1.50 | 75.0% | 150% | o mesmo crescimento que a metade, mas o triplo do risco |

| 2.00 (dobro) | 0.0% | 200% | sem crescimento, risco máximo |

| > 2.00 | negativo | — | ruína apesar de um edge positivo |

Três conclusões:

- O meio Kelly captura 75% do crescimento com metade da volatilidade. Em termos de risco/retorno, isso é muito melhor do que o Kelly completo.

- A parábola é simétrica em torno de . Apostar Kelly dá o mesmo crescimento que , mas é três vezes mais volátil. Exceder é punido com mais severidade do que ficar aquém.

- Em Kelly o crescimento vai a zero, e além disso torna-se negativo. Um dimensionamento demasiado agressivo mata o capital mesmo numa estratégia vencedora.

Os drawdowns do Kelly completo: a fórmula que traz de volta à realidade

Para o modelo contínuo, a probabilidade de o capital cair alguma vez a uma fração do seu valor inicial é igual a:

Insira os níveis de Kelly — e obtém-se uma tabela após a qual o Kelly completo deixa de parecer atraente:

| Multiplicador | P(alguma vez −50%) | P(alguma vez −75%) |

|---|---|---|

| 1.00 (completo) | 50% | 75% |

| 0.50 (metade) | 12.5% | 1.6% |

| 0.25 (quarto) | 0.78% | 0.006% |

| 2.00 (dobro) | 100% | 100% |

Com o Kelly completo, a probabilidade de sofrer alguma vez um drawdown de 50% é de 50%. Isto não é um cenário de cauda — é jogar uma moeda ao ar. O meio Kelly reduz para 12.5%, o quarto de Kelly para uma fração de percentual. E isso é num modelo gaussiano idealizado; as caudas pesadas reais tornam os drawdowns reais ainda mais profundos.

A calculadora: mova a fração de Kelly — observe o retorno e o risco

Mova os controles deslizantes. Os dois superiores definem o edge da estratégia (probabilidade de vitória e relação de pagamento), o inferior define o multiplicador de Kelly . Observe como a taxa de crescimento do capital e a probabilidade de um drawdown profundo mudam simultaneamente. Preste atenção ao gráfico principal do artigo: ao passar de meio para Kelly completo, o crescimento sobe um pouco, enquanto o risco de drawdown sobe várias vezes.

Brinque com o controle deslizante da fração de Kelly ao redor dos valores 0.5 e 1.0: o crescimento em relação ao máximo sobe de 75% para 100%, mas o risco de um drawdown de 50% salta de 13% para 50%. É exatamente por isso que os profissionais vivem na metade esquerda da parábola.

O Kelly fracionário como padrão da indústria

Gestores sérios quase nunca apostam no Kelly completo. O intervalo típico vai de a Kelly. Além dos drawdowns, há quatro razões fundamentais para reduzir a fração.

1. Erro na estimativa dos parâmetros. A fórmula assume que você conhece os valores verdadeiros de , , , . Na realidade, você os estima a partir de uma amostra finita. E a função de crescimento é assimétrica: superestimar o edge empurra você além do ótimo, onde o crescimento cai mais rápido do que sobe com a mesma subestimação. Se o Kelly verdadeiro é igual a e você o estimou com erro, é mais seguro apostar sistematicamente menos. Regra prática: quando a estimativa é incerta, corte a fração pela metade.

2. Não estacionariedade. O edge de uma estratégia não é uma constante — os regimes de mercado mudam, o edge se deteriora, os concorrentes copiam a ideia. O Kelly calculado com os dados de ontem pode se mostrar superestimado amanhã. Um multiplicador fracionário é um amortecedor contra a deterioração do edge.

3. Caudas pesadas. A fórmula gaussiana subestima o risco de movimentos extremos. Em distribuições reais de cauda pesada, ela aposta demais de forma sistemática. O Kelly fracionário compensa parcialmente isso.

4. O custo dos drawdowns em um negócio. Para um market maker, um drawdown não é apenas psicologia. São chamadas de margem, reduções forçadas de posição no pior momento possível, saídas de capital de investidores, um custo de financiamento crescente (veja Como as taxas de financiamento matam a alavancagem). Uma curva de patrimônio suave tem um valor próprio que está ausente da fórmula de Kelly.

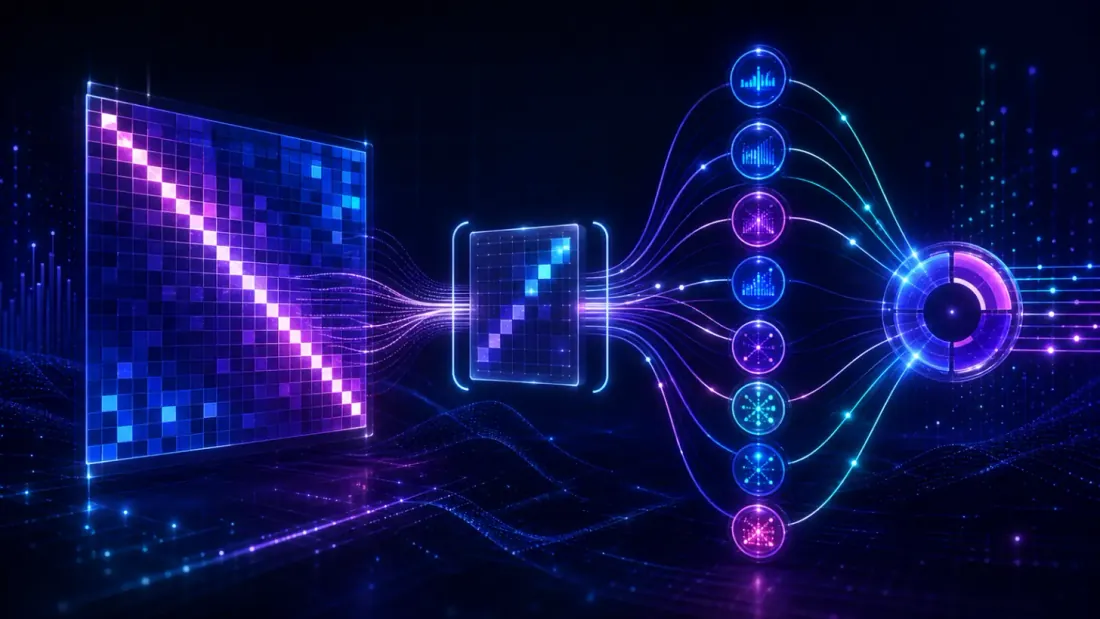

Kelly para uma carteira de estratégias

Até agora falamos sobre uma única estratégia. Mas a verdadeira questão é escolher o Kelly para estratégias no plural: você tem várias estratégias e precisa alocar capital entre elas.

A abordagem ingênua — calcular o Kelly para cada uma separadamente e somá-las — está catastroficamente errada, porque ignora as correlações. Duas estratégias fortemente correlacionadas são essencialmente uma única aposta duplicada, e o risco total deve ser contado como se fosse de uma só.

A forma matricial

Para um vetor de retornos esperados e uma matriz de covariância , o vetor ótimo de frações para todas as estratégias de uma vez:

A taxa de crescimento no ótimo generaliza-se para o quadrado do Sharpe da carteira:

Note: é a direção da carteira de Sharpe máximo (a carteira tangente). Kelly e otimização média-variância são dois lados da mesma moeda: o Kelly simplesmente fixa o nível de alavancagem que maximiza o crescimento geométrico.

O que a covariância inversa faz

- Estratégias correlacionadas compartilham o orçamento de risco. Se duas estratégias são quase idênticas, a matriz reduzirá sua fração combinada ao nível de uma só — automaticamente, sem gambiarras manuais.

- Estratégias não correlacionadas recebem um prêmio de diversificação. Podem ser mantidas mais próximas de seus tamanhos individuais, e o Sharpe total da carteira será maior do que cada uma separadamente.

- Estratégias correlacionadas negativamente podem receber frações aumentadas — elas se protegem mutuamente, e a matriz recompensa isso.

Um alerta sobre a estimativa de

Inverter uma matriz de covariância é numericamente instável: em estimativas ruidosas, infla pequenos erros em pesos descontrolados. A contração (shrinkage) da covariância em direção à diagonal, os limites de alavancagem e o mesmo multiplicador fracionário são obrigatórios. Sem eles, o Kelly matricial produz frações que parecem lindas no backtest e letais na produção.

Ajustes para trading algorítmico e market making

A fórmula pura vive em um mundo estéril. Em um motor real, você precisa de ajustes.

- Comissões e slippage reduzem o edge efetivo. Calcule o Kelly sobre os retornos após todos os custos, senão você apostará demais de forma sistemática.

- A discretização das apostas e o tamanho dos lotes impedem você de apostar exatamente — arredonde para baixo, não para cima.

- Um edge não estacionário exige recálculo ao longo do tempo: estimativas de e em uma janela móvel com meia-vida, não sobre todo o histórico.

- Uma restrição de drawdown. Além do Kelly, defina um teto rígido: drawdown máximo, alavancagem máxima, fração máxima por estratégia individual. Existem versões formais de Kelly com restrição de drawdown (Busseti, Boyd), mas na prática um limite simples é suficiente.

- Honestidade ao estimar o edge. O principal erro é alimentar o Kelly com um edge medido in-sample. Use apenas uma estimativa out-of-sample, em walk-forward, após comissões. Um edge superestimado que entra na fórmula significa uma aposta superestimada que sai.

A receita: como aplicar isso

- Estime o edge honestamente. Out-of-sample, em walk-forward, após comissões e slippage. Esta é a etapa mais importante — lixo entra, ruína sai.

- Calcule o Kelly completo. Binário para resultados discretos ou contínuo para retornos.

- Tome uma fração. Por padrão, – do Kelly completo. Quanto menos robusto o edge, menor o multiplicador.

- Para uma carteira, calcule em forma matricial. com contração de covariância, depois o mesmo multiplicador fracionário.

- Defina limites rígidos. Máximo por posição, alavancagem máxima, um limite de drawdown — além de tudo o mais.

- Recalcule. À medida que as estimativas se atualizam, reduza a fração quando a incerteza aumentar e o edge se deteriorar.

Código

import numpy as np

def kelly_binary(p, b):

"""p — win probability, b — net payout ratio per 1 unit of stake."""

q = 1 - p

return (b * p - q) / b # = p - q/b

def kelly_continuous(mu, sigma):

"""mu, sigma — mean and standard deviation of period returns (in the same units)."""

return mu / sigma ** 2

def kelly_portfolio(mu, cov, shrink=0.0):

"""Matrix Kelly for a portfolio of strategies.

mu — vector of expected returns;

cov — covariance matrix of returns;

shrink — shrinkage coefficient toward the diagonal (0..1) for stable inversion."""

cov = np.asarray(cov, float)

if shrink:

cov = (1 - shrink) * cov + shrink * np.diag(np.diag(cov))

return np.linalg.solve(cov, np.asarray(mu, float))

def sized(f_star, kelly_fraction=0.25, cap=0.2):

"""Fractional Kelly with a hard cap on the fraction."""

return float(np.clip(f_star * kelly_fraction, -cap, cap))

f = kelly_binary(p=0.55, b=1.0) # 0.10 — full Kelly

print(sized(f)) # 0.025 — quarter Kelly, a safe size

Erros comuns

- Kelly sobre um edge in-sample. O erro mais caro. Um edge superestimado → aposta excessiva → crescimento negativo.

- Ignorar as correlações entre estratégias. A soma dos Kelly individuais não é o Kelly da carteira.

- Kelly completo em produção. O máximo matemático de crescimento, mas 50% de chance de um drawdown até a metade da conta. Não se encaixa em quase ninguém.

- Kelly com um edge instável. Se o edge se deteriora, a fórmula superestima sistematicamente a aposta.

- Confundir objetivos. O Kelly maximiza o crescimento geométrico do capital — não o Sharpe, não a probabilidade de permanecer no positivo, e não o conforto. Se uma curva suave importa mais para você, aposte deliberadamente no Kelly fracionário.

Conclusão

O critério de Kelly responde à pergunta central de qualquer estratégia — quanto apostar — com uma fórmula que maximiza o crescimento geométrico de longo prazo: para apostas e para retornos, e para uma carteira — .

Mas o Kelly completo é o ótimo matemático para o crescimento, não para a sobrevivência. O Kelly fracionário (–) captura a maior parte do crescimento com uma volatilidade e drawdowns várias vezes menores. Então, a resposta prática para a questão de escolher o Kelly para estratégias é a seguinte: calcule o Kelly completo com honestidade — mas aposte uma fração dele, além de limites rígidos de risco.

Material relacionado:

Authors

Trading-systems engineer

Trading-systems engineer building bots since 2017: cross-exchange arbitrage (connected up to 30 venues), cointegration-based pairs arbitrage across spot and futures, scalping, news and sentiment-driven strategies, trend algorithms, and portfolio management and balancing algorithms. Also builds sub-millisecond order execution, big-data warehouses, backtesting engines, AI agents, and trading interfaces (incl. open-source profitmaker.cc). Stack: JS/TS, Python, Rust/Zig/Go, DevOps, backend, frontend, architecture.

Read More

Assimetria Perda-Lucro: A Matemática que Destrói o seu Depósito

Teoria de Portfólio de Markowitz para Cripto: Do Zero ao Herói