Sun'iy intellekt savdo tahlillari, bozor tahlili va platforma yangiliklari uchun bizning xabarnomaga obuna bo'ling.

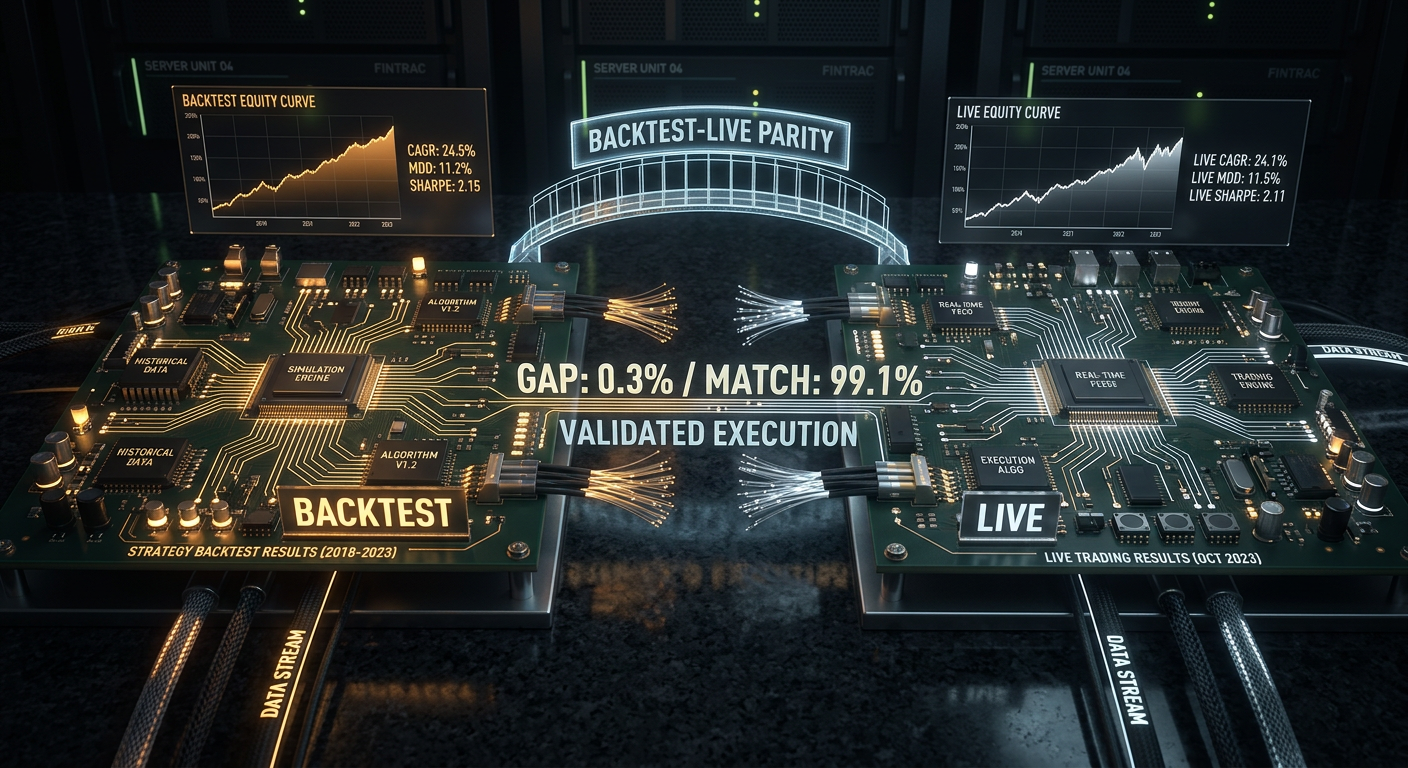

You ran a strategy through a backtest. Sharpe 2.1, MaxDD -8%, PnL +67%. You launched the bot. A month later you compare: the same signals, the same period — but live PnL is 40% lower. The drawdown is one and a half times deeper. Two out of ten trades were not executed at all.

This is not a bug. This is backtest-live divergence — a systematic discrepancy between backtest results and real trading. Everyone has it. The only question is whether you know about it and whether you can control it.

This article provides a complete taxonomy of divergences, architectural patterns for minimizing them, and a practical checklist for monitoring parity in production.

The "it worked in backtest" syndrome

Every algotrader goes through this cycle:

Wrote a strategy in a Jupyter notebook

Ran a backtest on historical CSV — results are great

Rewrote the logic as a bot (often in a different language or framework)

Launched — results do not match

Started looking for a bug, did not find one — "the market changed"

The problem is not the market. The problem is that the backtest and the bot are two different software products that model the same reality differently. Divergences are inevitable, but they can be systematized and minimized.

Taxonomy of Divergences

All sources of divergence fall into four categories. For each one — a severity rating (from 1 to 5) and a typical contribution to PnL divergence.

1. Data divergences (severity: 3/5)

The data the backtest sees and the data the bot sees in real time are not the same thing.

Timestamps. Exchanges deliver candles with different rules for timestamp assignment. One exchange marks the candle with the start of the period, another with the end. A REST API may return a candle with a 1-3 second delay after the actual close. The backtest works with "ideal" timestamps from the historical file.

OHLCV aggregation. Historical data is often aggregated by the provider differently than the exchange does in real time. The difference is in the last digit — but with threshold signals (MA crossover, level breakout) this determines whether the strategy enters a position or not.

Gaps and missing data. Historical data is usually clean — missing candles are filled by interpolation. In real time, a WebSocket may drop, and the bot misses 30 seconds of data.

Typical contribution to PnL divergence: 2-5% of annual PnL.

2. Execution divergences (severity: 5/5)

The most dangerous class of divergences. The backtest simulates execution perfectly — reality is far from ideal.

Slippage. The backtest fills the order at the close price (or the signal price). In reality, a market order is executed at the best bid/ask plus slippage that depends on volume and liquidity. For a $10K position on a mid-liquidity altcoin, slippage can be 0.05-0.3%.

Formula for cumulative slippage over N trades:

Slippagetotal=∑i=1Nsizei×si

where si is the slippage of the i-th trade, depending on orderbook depth:

si≈Liquidity(ti)sizei×k

Latency. From the moment a signal is generated to order execution, time passes: signal computation (1-50 ms), request transmission (10-200 ms), matching on the exchange (1-10 ms). In the backtest, latency = 0. In live — the price can move.

Partial fills. The backtest assumes 100% of the order is filled instantly. In reality, a limit order may be partially filled — or not filled at all if the price reverses. For a market order on an illiquid market, the order "slips" through multiple orderbook levels.

Queue priority. A limit order placed at the best bid price will not be filled immediately — it queues behind all previously placed orders at that level. A backtest that considers "price touched = order filled" systematically overstates the fill rate.

Typical contribution to PnL divergence: 10-30% of annual PnL.

3. Logic divergences (severity: 4/5)

These are divergences in the strategy code itself between the backtest and the bot.

Separate codebases. The classic anti-pattern: backtests/strategy_a.py and bot/strategy_a.py — two separate files that "do the same thing." After three months of edits, they inevitably diverge. Someone added a filter in the backtest and forgot to replicate it in the bot. Or the opposite — a bug was fixed in the bot but remained in the backtest.

Different frameworks. Backtest on pandas with vectorized operations, bot on asyncio with event-driven logic. Even with an identical strategy, edge cases are handled differently: rounding, order of condition checks, NaN handling.

State management. The backtest is usually stateless — it iterates over a data array. The bot is stateful — it stores positions, balances, order history. Bot restart, state loss, desynchronization with the exchange — all of these are sources of divergence.

Typical contribution to PnL divergence: 5-20% of annual PnL.

4. Cost divergences (severity: 3/5)

Divergences in trading cost modeling.

Funding rates. Most perpetual futures backtests do not account for funding rates at all. At 10x leverage and an average rate of 0.01% per 8 hours, this is 0.01%×3×365×10=109.5% per year — more than the PnL of most strategies. A detailed analysis is in the article Funding rates kill your leverage.

Commissions. Maker/taker commissions are usually modeled but often with the wrong rate. VIP tiers, BNB discounts, rebates — all of these affect the final result.

Spread. A candle-based backtest does not see the bid-ask spread. On a 1-minute candle, close = 3000, but in reality bid = 2999.5 and ask = 3000.5. Each trade "costs" half the spread.

Typical contribution to PnL divergence: 5-15% of annual PnL.

Cumulative Effect

All four categories act simultaneously and, as a rule, in one direction — against the trader:

A total divergence of 20-50% from backtest PnL is normal for an unrefined system. With leverage, the effect is multiplied.

Architectural Patterns for Parity

Pattern 1: Shared Core (extracting a common core)

The idea: extract the strategy core — signal generation and execution logic — into a separate module used by both the backtest and the bot. Only the surrounding infrastructure differs: the data source and the order submission mechanism.

from dataclasses import dataclass

from typing importOptionalimport numpy as np

@dataclassclassSignal:

side: str# 'long' | 'short'

entry_price: float

sl_price: float

tp_price: float

size: float

timestamp: int@dataclassclassOrderRequest:

side: str

order_type: str# 'market' | 'limit'

price: float

size: floatclassStrategyCore:

"""

Strategy core. Identical code for backtest and live.

Depends only on data, not on infrastructure.

"""def__init__(self, params: dict):

self.fast_period = params.get('fast_ma', 20)

self.slow_period = params.get('slow_ma', 50)

self.sl_pct = params.get('sl_pct', 0.02)

self.tp_pct = params.get('tp_pct', 0.04)

self.position: Optional[Signal] = Noneself._closes: list[float] = []

defon_candle(self, timestamp: int, o: float, h: float,

l: float, c: float, v: float) -> Optional[OrderRequest]:

"""

Process a new candle. Returns an OrderRequest or None.

This method is called identically from the backtest and the bot.

"""self._closes.append(c)

iflen(self._closes) < self.slow_period:

returnNone

fast_ma = np.mean(self._closes[-self.fast_period:])

slow_ma = np.mean(self._closes[-self.slow_period:])

ifself.position isnotNone:

exit_order = self._check_exit(h, l, c)

if exit_order:

self.position = Nonereturn exit_order

ifself.position isNone:

if fast_ma > slow_ma andself._prev_fast_ma <= self._prev_slow_ma:

self.position = Signal(

side='long', entry_price=c,

sl_price=c * (1 - self.sl_pct),

tp_price=c * (1 + self.tp_pct),

size=1.0, timestamp=timestamp,

)

return OrderRequest('buy', 'market', c, 1.0)

self._prev_fast_ma = fast_ma

self._prev_slow_ma = slow_ma

returnNonedef_check_exit(self, high: float, low: float,

close: float) -> Optional[OrderRequest]:

pos = self.position

if pos.side == 'long':

if low <= pos.sl_price:

return OrderRequest('sell', 'market', pos.sl_price, pos.size)

if high >= pos.tp_price:

return OrderRequest('sell', 'market', pos.tp_price, pos.size)

returnNone

Now the backtest and the bot use the same StrategyCore:

from strategy_core import StrategyCore

defrun_backtest(candles, params, fill_model):

core = StrategyCore(params)

trades = []

for candle in candles:

order = core.on_candle(

candle['timestamp'], candle['open'], candle['high'],

candle['low'], candle['close'], candle['volume'],

)

if order:

fill_price = fill_model.simulate_fill(order, candle)

trades.append({'price': fill_price, 'side': order.side})

return trades

from strategy_core import StrategyCore

asyncdefrun_live(exchange, symbol, params):

core = StrategyCore(params)

asyncfor candle in exchange.stream_candles(symbol, '1m'):

order = core.on_candle(

candle['timestamp'], candle['open'], candle['high'],

candle['low'], candle['close'], candle['volume'],

)

if order:

await exchange.place_order(symbol, order.side,

order.order_type, order.size)

The key rule: StrategyCore does not know where data comes from or where orders are sent. It receives OHLCV and returns an OrderRequest. Everything else is the responsibility of the infrastructure layer.

NautilusTrader implements parity through a unified NautilusKernel — a Rust-native engine with a deterministic event-driven core and nanosecond resolution. The same strategy implementation works in both the backtest and live trading.

The architecture is built on the ports and adapters pattern (hexagonal architecture):

Freqtrade uses a unified IStrategy interface: the same strategy class works in both the backtest and live. The only difference is the persistence layer.

classIStrategy:

"""Unified interface — the implementation does not know if this is a backtest or live."""defpopulate_indicators(self, dataframe, metadata):

"""Compute indicators."""

dataframe['fast_ma'] = dataframe['close'].rolling(20).mean()

dataframe['slow_ma'] = dataframe['close'].rolling(50).mean()

return dataframe

defpopulate_entry_trend(self, dataframe, metadata):

"""Determine entry signals."""

dataframe.loc[

(dataframe['fast_ma'] > dataframe['slow_ma']) &

(dataframe['fast_ma'].shift(1) <= dataframe['slow_ma'].shift(1)),

'enter_long'

] = 1return dataframe

defpopulate_exit_trend(self, dataframe, metadata):

"""Determine exit signals."""

dataframe.loc[

(dataframe['fast_ma'] < dataframe['slow_ma']),

'exit_long'

] = 1return dataframe

Freqtrade additionally provides:

Hyperopt via Optuna — strategy parameter optimization

--timeframe-detail — drill-down to a finer timeframe for fill refinement (similar to adaptive drill-down)

Pattern Comparison

Shared Core

Event-driven (NautilusTrader)

Strategy Interface (Freqtrade)

Implementation complexity

Low

High

Medium

Parity level

Medium

Maximum

High

Fill simulation

Separate FillModel

L2 orderbook

--timeframe-detail

Core language

Python

Rust + Python

Python

Suitable for

Custom engines

Institutional trading

Quick start

Fill Simulation Accuracy

Fill simulation is the main source of execution divergence. Three levels of accuracy:

Level 1: Naive (fill at close price)

fill_price = candle['close']

Error: does not account for slippage, spread, or partial fills. Systematically overstates PnL.

Level 2: Slippage model

defsimulate_fill(order, candle, slippage_bps=5):

"""Fill with slippage."""

base_price = candle['close']

slip = base_price * slippage_bps / 10000if order.side == 'buy':

return base_price + slip # Buy at a higher priceelse:

return base_price - slip # Sell at a lower price

Error: fixed slippage does not account for liquidity and order size. Better than naive, but still a crude model.

Market impact formula (simplified Almgren-Chriss model):

Δp=σ⋅k⋅VmarketVorder

where σ is volatility, k is the impact coefficient, Vorder is the order volume, and Vmarket is the market volume for the period.

Practical Parity Checklist

Before launching the bot live, verify each item:

Code:

Strategy uses a shared core (one module for backtest and live)

No duplication of signal logic in two places

Unit tests verify identical core outputs for identical inputs

Order of condition checks is identical (SL before TP? TP before SL?)

Data:

Timestamp format is identical (UTC, same provider)

OHLCV aggregation uses the same rules

Missing candle handling is identical

No look-ahead bias — the backtest does not peek into the future

Execution:

Slippage model is calibrated on real data

Partial fills are modeled (or at least pessimistically estimated)

Limit orders have a queue priority model

Latency is accounted for (100-500 ms delay from signal to fill)

Costs:

Maker/taker commissions are included with the current rate

Funding rates are accounted for with perpetual futures

Spread is modeled (at least the average)

Infrastructure:

State persistence: the bot recovers positions after restart

Reconnection logic: WebSocket reconnects without data loss

Logging: all orders and fills are logged for post-mortem analysis

Monitoring Divergence in Production

Parity is not a one-time check but a continuous process. After launching the bot, divergences must be tracked in real time.

Shadow mode (paper trading)

Run the bot in parallel with the backtest on the same data. The bot generates signals but does not send orders — it only logs. Simultaneously, the backtest processes the same data. Compare:

classDivergenceMonitor:

"""

Compares backtest and live bot signals in real time.

"""def__init__(self, tolerance_pct=0.5):

self.tolerance = tolerance_pct / 100self.divergences = []

defcompare_signal(self, backtest_signal, live_signal, timestamp):

"""Compare backtest and live signals."""if backtest_signal isNoneand live_signal isNone:

return# Both silent — OKif (backtest_signal isNone) != (live_signal isNone):

self.divergences.append({

'timestamp': timestamp,

'type': 'signal_mismatch',

'backtest': backtest_signal,

'live': live_signal,

'severity': 'HIGH',

})

return

price_diff = abs(

backtest_signal.entry_price - live_signal.entry_price

) / backtest_signal.entry_price

if price_diff > self.tolerance:

self.divergences.append({

'timestamp': timestamp,

'type': 'price_divergence',

'diff_pct': price_diff * 100,

'severity': 'MEDIUM',

})

defcompare_fill(self, backtest_fill, live_fill, timestamp):

"""Compare execution."""if backtest_fill and live_fill:

slippage = (live_fill['price'] - backtest_fill['price']

) / backtest_fill['price']

self.divergences.append({

'timestamp': timestamp,

'type': 'fill_divergence',

'slippage_bps': slippage * 10000,

'severity': 'LOW'ifabs(slippage) < 0.001else'MEDIUM',

})

defreport(self):

"""Weekly divergence report."""from collections import Counter

severity_counts = Counter(d['severity'] for d inself.divergences)

return {

'total_divergences': len(self.divergences),

'by_severity': dict(severity_counts),

'avg_slippage_bps': np.mean([

d['slippage_bps'] for d inself.divergences

if d['type'] == 'fill_divergence'

]) ifany(d['type'] == 'fill_divergence'for d inself.divergences) else0,

}

Dashboard Metrics

Metric

Formula

Alert Threshold

Signal match rate

total signalsmatches

< 95%

Avg slippage

N1∑si (bps)

> 10 bps

Fill rate

sentfilled

< 90%

PnL divergence

PnLbtPnLlive−PnLbt

> 20%

Latency p99

99th percentile signal-to-fill

> 500 ms

Slippage Model Calibration

After accumulating data for 2-4 weeks, you can calibrate the backtest slippage model on real data:

defcalibrate_slippage(live_fills: list[dict]) -> dict:

"""

Calibrate slippage model using real fills.

live_fills: [{'expected_price': ..., 'actual_price': ..., 'size_usd': ..., 'volume_usd': ...}]

"""

slippages = []

participation_rates = []

for fill in live_fills:

slip = abs(fill['actual_price'] - fill['expected_price']

) / fill['expected_price']

part = fill['size_usd'] / max(fill['volume_usd'], 1)

slippages.append(slip)

participation_rates.append(part)

slippages = np.array(slippages)

participation_rates = np.array(participation_rates)

from scipy.optimize import curve_fit

defmodel(x, k, base):

return k * np.sqrt(x) + base

popt, _ = curve_fit(model, participation_rates, slippages,

p0=[0.1, 0.0001])

return {

'impact_coeff': popt[0],

'base_slippage': popt[1],

'mean_slippage_bps': np.mean(slippages) * 10000,

'p95_slippage_bps': np.percentile(slippages, 95) * 10000,

}

Connections with Other Tools

Backtest-live parity is not an isolated task. It intersects with other tools from the "Backtests Without Illusions" series:

Adaptive drill-down — improves fill simulation accuracy, a key component of execution parity.

Funding rates — if the backtest does not model funding, parity is impossible at leverage > 3x.

Parquet cache — precomputed timeframes and indicators ensure that the backtest sees the same data as the bot. RunningCandleBuffer emulation = real-time updating.

Polars vs Pandas — when switching from pandas (backtest) to Polars (live), you need to ensure that numerical results match.

Walk-Forward — walk-forward on out-of-sample data shows how the strategy degrades — this is closer to live than an in-sample backtest.

Recommendations

Shared core is mandatory. A single codebase for signal generation is the minimum requirement for parity. Two files with identical logic guarantee divergence within a month.

Calibrate the fill model. A fixed 5 bps slippage is better than nothing. A slippage model calibrated on real data is significantly better.

Use shadow mode for the first 2-4 weeks. Do not trade with real money until the signal match rate reaches 95%+.

Model funding rates. For perpetual futures, this is not optional — it is mandatory. Funding can consume all PnL at leverage > 5x.

Log everything. Every signal, every order, every fill — with timestamps. Without logs, post-mortem analysis is impossible.

Automate the comparison. A weekly DivergenceMonitor report should arrive automatically. Do not wait until PnL goes negative.

Pessimistic backtest by default. It is better to underestimate expectations in the backtest and be pleasantly surprised in live than the reverse. The slippage model should be conservative.

Conclusion

Backtest-live parity is not a property of a system but a process. Perfect parity does not exist: a backtest is by definition a model of reality, and a model always simplifies. But the difference between "the model differs by 5%" and "the model differs by 50%" is determined by architecture.

@article{soloviov2026backtestliveparity,

author = {Soloviov, Eugen},

title = {Backtest-live parity: why your bot trades differently from the backtest},

year = {2026},

url = {https://marketmaker.cc/ru/blog/post/backtest-live-parity},

description = {Complete taxonomy of divergences between backtesting and live trading: from slippage and partial fills to codebase desynchronization. Architectural patterns for achieving parity and a production monitoring checklist.}

}