Daily Stock Analysis: Байкоо тизмесин күндөлүк чечим кабыл алуу панелине айландырган AI система

ZhuLinsen жазган daily_stock_analysis долбоору азыркы учурдагы эң көп жылдызга ээ AI-финансы долбоорлорунун бири — Trendshift боюнча күндүн №1 Python репозиторийи. Бирок кызыктуусу жылдыздардын саны эмес. Долбоор баалардын өзгөрүшүн болжолдойт деп жасалма кыялданбайт. Тескерисинче, ал тардыраак, бирок алда канча пайдалуу маселени чечет: ар бир соода күнү байкоо тизмеңизди алып, структураланган, түшүндүрмөлүү аналитикалык отчет жасайт — жана аны чын эле окуй турган жериңизге, мессенжериңизге жеткирет.

Долбоордун автору тарабынан эскертүү: окуу жана изилдөө үчүн гана. Бул инвестициялык кеңеш эмес. Рынокторго тобокелдик мүнөздүү.

Негизги идея: бот эмес, күндөлүк аналитик-репортер

Көпчүлүк "AI trading" репозиторийлери бирдей кыялдын артынан жүрүшөт: модель кирет, сигнал чыгат, акча көбөйөт. daily_stock_analysis андан ак ниеттүү негизде курулган — инвестициянын кыйын бөлүгү дагы бир сигнал чыгаруу эмес, тескерисинче, актив тууралуу толук, ырааттуу сүрөттү чогултуу жана аны күн сайын бирдей түрдө жазуу.

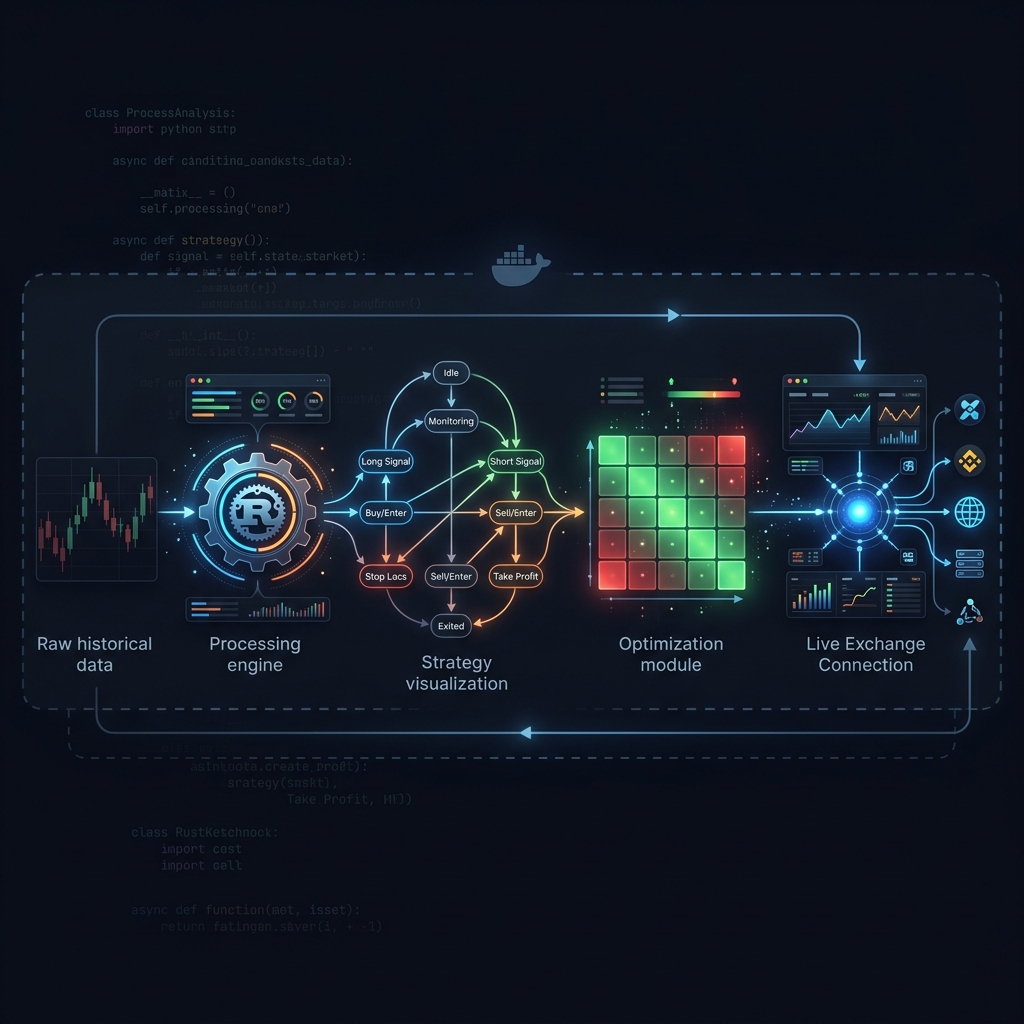

Ошондуктан ал график боюнча иштеген жаш аналитик сыяктуу иштейт. Түтүк (pipeline) сызыктуу жана түшүнүктүү:

| Этап | Эмне болот |

|---|---|

| Маалымат алуу | Котировкалар, күндөлүк шамдар, индикаторлор, капитал агымы, фундаменталдык көрсөткүчтөр, "chips" |

| Техникалык анализ | Жылышкан орточолор, RSI, көлөм, bias катышы, тренддин классификациясы |

| Жаңылыктар жана акыл-эс | Акыркы жаңылыктарды, жарыяларды, ар бир тикер боюнча маанайды издейт |

| LLM анализи | Контекст пакетин жана промптту түзөт, JSON форматындагы чечим панелин чыгарат |

| Отчетту жаратуу | Markdown отчету, кааласа сүрөткө айландырылат |

| Билдирүү | WeCom, Feishu, Telegram, Discord, Slack же электрондук почтага жөнөтөт |

Демейки боюнча ал график боюнча иштейт (жумуш күндөрү, рынок жабылгандан кийин) жана соода болбогон күндөрдү өткөрүп жиберет. Ал A-акцияларды, Гонконгду, АКШ акцияларын жана ETF'лерди камтыйт, ал эми Япония менен Кореянын рынокторуна маалымат булактары жетпеген жерде төмөндөтүлгөн деңгээлде колдоо көрсөтүлөт.

Тынч гана акылдуу бөлүк: маалымат fallback

Долбоордогу эң берик инженердик чечим LLM эмес — бул маалыматты демейки боюнча ишенимсиз деп кароо.

Рынок маалыматы алты жеткирүүчүнүн приоритеттик чынжыры аркылуу алынат, ар бирөө мурункусуна fallback катары кызмат кылат:

Efinance (P0) → Tencent (P0) → Akshare (P1) → Pytdx (P2) → Baostock (P3) → Yfinance (P4)

АКШ тикерин анализдегенде, система автоматтык түрдө Кытайга гана арналган жеткирүүчүлөрдү өткөрүп жиберип, Yahoo Finance'ке багыттайт. Эгер булак иштебей калса, убакыт бүтсө же жарым-жартылай маалымат кайтарса, run бүт отчетту кыйраткандын ордуна ошол блокту гана начарлатат. Промптко атүгүл кайсы блоктор fallback, partial же missing экени айтылат — ошондуктан модель бир сандын оюп чыгарбастан "маалымат жеткиликсиз" деп жазууга милдеттүү.

Бул ар кандай production системасы үчүн туура интуиция: бир маалымат булагынын иштебей калышы бүт анализди кыйраткыс болбошу керек. Ар бир агымды эң мыкты аракет (best-effort) катары карап, талааларды стандартташтырып, жоголгон маалыматты үнсүз толтуруунун ордуна көрүнөрлүк кылуу керек.

Чечим панели

LLM проза кайтарбайт — ал катуу структураланган JSON "чечим панелин" кайтарат, отчет аны ырааттуу макетке айландырат:

- Негизги корутунду — бир сүйлөм: сатып алуу, кармап туруу же күтүү, ошондой эле убакыттын сезгичтиги.

- Бөлүнгөн кеңеш — позицияны кармап тургандар менен накталай акчасы барлар үчүн ар кандай көрсөтмө.

- Маалымат перспективасы — MA тегиздигинин абалы, баа менен колдоо/каршылык деңгээлдеринин катышы, bias катышы, көлөмдүн окулушу.

- Акыл-эс — тобокелдик эскертүүлөрү жана позитивдүү катализаторлор, ар бирине дата талап кылынат.

- Салгылашуу планы — так снайпер чекиттери: идеалдуу сатып алуу, stop-loss, максат, позиция көлөмү.

- Текшерүү тизмеси — ар бир шарт ✅ / ⚠️ / ❌ менен белгиленет (бычак тегиздиги, bias диапазону, көлөм, чоң терс жаңылыктардын жоктугу, баалоо).

Промптко жазылган тартип таасирдүү жана акылга сыярлык: артынан кубалаба (MA5дан 5%дан ашык bias катуу "сатып алба" деген белги), MA тегиздиги гана бычак болгондо соода кыл (MA5 > MA10 > MA20), колдоого чейин көлөмү кичирейген артка тартылууну сатып алганды артык көр, жана бир күндүк кыймылга карата сатып алуу менен сатуунун ортосунда эч качан оодарылба.

Агент стратегиялары: системага суроо бер

Күндөлүк отчеттон тышкары, долбоор ар бир тикер боюнча суроо берүүгө боло турган 15 орнотулган стратегиялык плейбуктары менен агент режимин камтыйт:

| Топ | Мисалдар |

|---|---|

| Тренд / жылышкан орточолор | MA алтын кесилиши, бычак тренди |

| Структура теориясы | Chan (Zen) теориясы, Эллиот толкуну |

| Жүрүм-турум / ликвиддүүлүк | эмоция цикли, көлөм жарылуусу, түптүн көлөмү, кичирейген артка тартылуу |

| Катализатор / нарратив | ысык тема, окуяга негизделген, күтүүлөрдүн кайра баасын коюу |

| Сапат / өсүш | өсүш сапаты |

Ар бир стратегия өзүнүн эрежелери, талап кылынган куралдары жана баллдык тууралоолору бар өзүнчө YAML файлы — ошондуктан "акыл-эс" бир чоң промпттун ичине жашырылган эмес, тескерисинче конфигурацияланган жана текшерилүүчү.

Аны өзүн-өзү алдабай кантип окуу керек

Ушул сыяктуу ар кандай долбоорго ашыкча ишенип кетүү оңой. Ак ниеттүү баалоо текшерүү тизмеси:

- Жаңылык булагынын сапаты. Акыл-эс блогу сиз орнотуп койгон издөө провайдерлериңиздей гана жакшы — алар болбосо, маанай жана катализаторлор бош калат, отчет толугу менен техникалык анализге таянат.

- Детерминизм. LLM'дин чыгыштары ар башка болушу мүмкүн; бирдей тикер ар бир run сайын аздап башкача окулушу мүмкүн. Панелди туруктуу чындык эмес, структураланган пикир катары карагыла.

- Рынок боюнча камтуу. A-акциялардын тереңдиги (капитал агымы, chips, "dragon-tiger") маалымат жетпеген рынокторго ыраатуу түрдө

not_supportedабалына түшөт. - Маалыматтын жаңылыгы.

fallback/partialбелгилерин байкагыла — начарлаган киргизүүлөр промптто көрсөтүлгөндөй ишенимиңизди төмөндөтүшү керек. - Backtesting ≠ пайда. Отчет чечим кабыл алууга жардам, бирок текшерилген артыкчылык эмес.

Чектөөлөр жана ак ниеттүү баалоо

daily_stock_analysis эмне эмес:

- Аткаруу системасы эмес. Ал анализдейт жана билдирет; заказ жайгаштырбайт же ликвиддүүлүктү моделдебейт.

- Моделге көз каранды. Чыгыштын сапаты сиз колдонгон LLM'ге жараша болот.

- Издөөгө көз каранды. Жаңылык API ачкычтары болбосо, отчеттун сапаттык бөлүгү жукарат.

- Детерминдик эмес. Бирдей киргизүүлөр аздап башкача панелдерди берүүсү мүмкүн.

Шилтемелер

- 💻 GitHub: ZhuLinsen/daily_stock_analysis

- 📄 Лицензия: MIT

Корутунду

daily_stock_analysis оракул катары эмес, тескерисинче автоматташтырылган, кайталанма аналитикалык адат катары баалуу:

- Акцияга "карап чыгуу" деген эмне экенин күн сайын стандартташтыруу.

- Маалыматты ишенимсиз деп кароо жана боштуктарды көрүнөрлүк кылуу.

- Корутундуну түшүндүрмөлүү кылуу — балл, деңгээлдер, текшерүү тизмеси, тобокелдиктер.

- Идея генерациялоону (15 стратегия) тартипке салынган чечим алкагынан бөлүү.

Окуу, күндөлүк карап чыгуу жана изилдөө агымын прототиптөө үчүн ал жакшы курулган. Production үчүн болсо, кийинки катмар ар бир олуттуу система талап кылган эле нерсе: текшерилген маалымат, моделдин четтөөсүн көзөмөлдөө, реалдуу аткаруу жана промпттордо гана эмес, кодто жашаган тобокелдик эрежелери.

Authors

Trading-systems engineer

Trading-systems engineer building bots since 2017: cross-exchange arbitrage (connected up to 30 venues), cointegration-based pairs arbitrage across spot and futures, scalping, news and sentiment-driven strategies, trend algorithms, and portfolio management and balancing algorithms. Also builds sub-millisecond order execution, big-data warehouses, backtesting engines, AI agents, and trading interfaces (incl. open-source profitmaker.cc). Stack: JS/TS, Python, Rust/Zig/Go, DevOps, backend, frontend, architecture.

Read More

AI Hedge Fund: жасалма интеллект талдоочулары бүтүмдөргө добуш берген көп агенттүү фонд

Kronos: шам графиктерин трансформер тилинде сүйлөшүүгө үйрөткөн негиз модели