AI Hedge Fund: A Multi-Agent Fund Where AI Analysts Vote on Trades

AI Hedge Fund is one of the most discussed open-source projects at the intersection of LLMs and trading. 12,000+ GitHub stars, hundreds of forks, enthusiastic Twitter posts. But strip away the hype and look soberly: the value isn't in "a neural network that makes money," but in an architectural pattern — how to organize a team of AI analysts so each contributes expertise without any single one blowing up the portfolio.

Disclaimer from the project author: This is not a system for real money — it's a sandbox for experiments.

Core Idea: Not One Guru, but a Committee

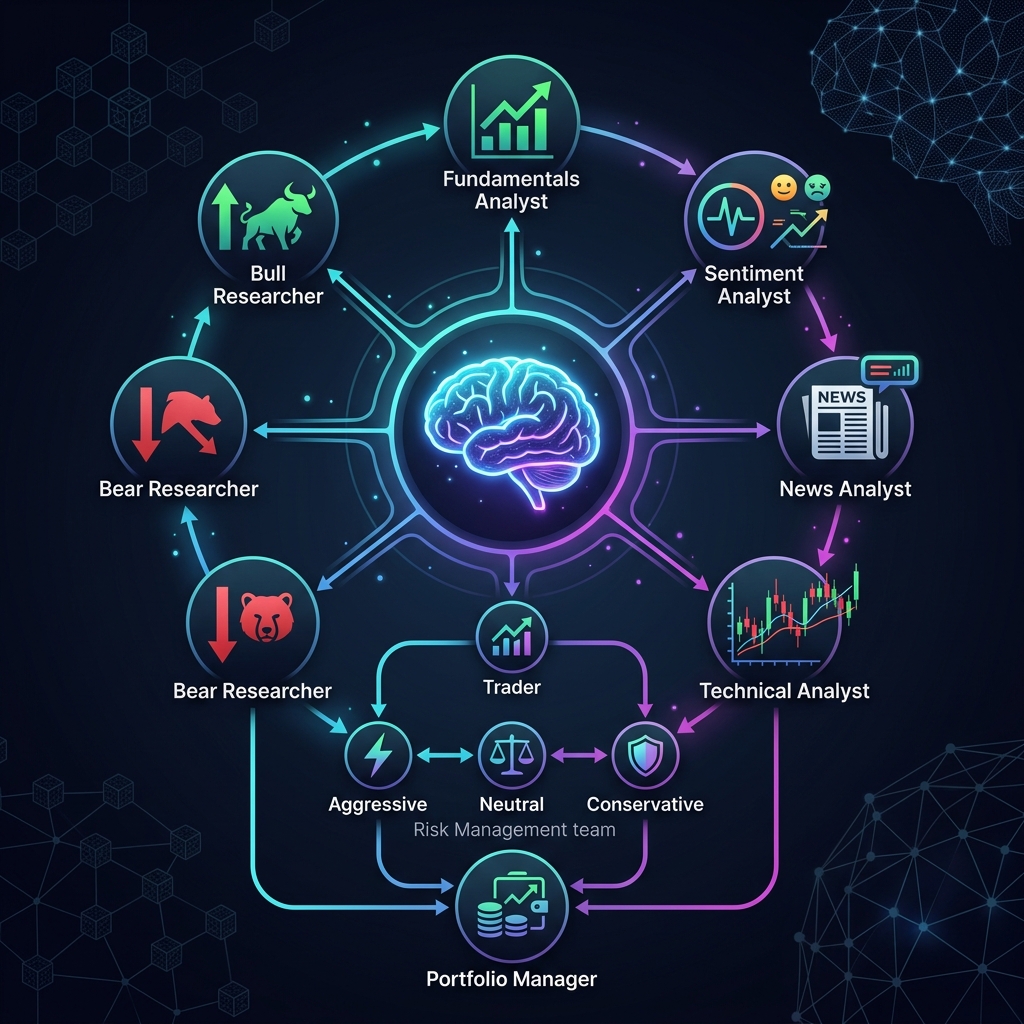

Most AI trading bots are simple: one LLM gets data → produces a signal → trade. AI Hedge Fund works fundamentally differently: it uses a team of agents with different thinking styles.

Each agent is a specialized LLM with its own prompt and data sources:

| Agent | Analysis Style | What It Examines |

|---|---|---|

| Value Analyst | Valuation | P/E, P/B, DCF, margins |

| Technical Analyst | Technical analysis | RSI, MACD, moving averages, levels |

| Sentiment Analyst | Market sentiment | News, social media, tone |

| Fundamentals Analyst | Fundamental analysis | Revenue, profit, debt, growth |

| Risk Manager | Risk control | Volatility, correlations, limits |

| Portfolio Manager | Final decision | Aggregates opinions, creates orders |

Agents work sequentially: first each analyst issues their assessment (buy/sell/hold with reasoning), then the risk manager checks permissibility, and only then does the portfolio manager form a specific action.

Why "Risk First, Action Second" Is Right

The strongest part of the project isn't "LLM magic" — it's the decision-making sequence.

The classic mistake in AI trading systems is giving the model complete freedom: "here's $100K, do whatever you want." AI Hedge Fund works differently:

-

Risk budget assessment. Before any agent proposes a trade, the system evaluates how much risk the portfolio can absorb — considering volatility, current positions, and asset correlations.

-

Size filtering. An agent can't "fantasize" a position for the entire deposit. If the limit allows only 5% — then only 5%, no matter how convincing the signal.

-

Opinion aggregation. The portfolio manager sees not just "buy/sell" but detailed arguments from each analyst. Diverging opinions aren't a bug — they're a feature: if the value analyst says "cheap" but the technical analyst says "downtrend," position size decreases.

In investing, what matters isn't just the signal, but the right to position size. This is the foundation-first approach: first a solid constraint framework, then "intelligence."

What This Gives in Practice

- Fewer chances for impulsive portfolio skews.

- Clear logic for why a trade size is what it is.

- More adequate backtesting experiments.

- Convenient ground for iterations: you can improve analysts without breaking the risk framework.

How to Read Results Without Self-Deception

Any project like this is easy to "overhype" if you only look at a pretty run. Here's an honest evaluation checklist:

- Stability across markets. Does it work in ranging markets as well as trending ones?

- Stress tests. What happens during panics, gaps, sharp reversals?

- Overfitting. Is the prompt logic tuned to specific tickers and periods?

- Data quality. Are commissions, slippage, and splits accounted for?

- Reproducibility. Will the same prompts give the same result in a week (LLMs are non-deterministic)?

Limitations and Honest Assessment

It's important to understand what AI Hedge Fund is not:

- Not a production system. No real execution, no liquidity modeling.

- LLM dependency. Decision quality is entirely determined by model quality. GPT-4 and GPT-3.5 will give different results.

- No historical backtest. You can't run the system on 5 years of data and get an equity curve.

- Determinism. LLMs with temperature > 0 will give different answers to identical inputs.

Links

- 💻 GitHub: virattt/ai-hedge-fund

- 📄 License: MIT

Conclusion

AI Hedge Fund is useful not as a "money-making machine" but as a thinking framework:

- Separate analyst roles.

- Separate idea generation from risk control.

- Make decisions explainable.

- Test hypotheses, but don't confuse backtesting with profit guarantees.

For learning and prototyping — solid work. For production, you need the next layer: realistic execution, data validation, model drift control, and a proper risk committee at the rules level, not just prompts.

Authors

Trading-systems engineer

Trading-systems engineer building bots since 2017: cross-exchange arbitrage (connected up to 30 venues), cointegration-based pairs arbitrage across spot and futures, scalping, news and sentiment-driven strategies, trend algorithms, and portfolio management and balancing algorithms. Also builds sub-millisecond order execution, big-data warehouses, backtesting engines, AI agents, and trading interfaces (incl. open-source profitmaker.cc). Stack: JS/TS, Python, Rust/Zig/Go, DevOps, backend, frontend, architecture.

Read More

Daily Stock Analysis: An AI System That Turns a Watchlist Into a Daily Decision Dashboard

algo-investor-skills: Claude Code Skills That Build a Scam-Proof Investor Proposal