Suscríbete a nuestro boletín para recibir información exclusiva sobre trading con IA, análisis de mercado y actualizaciones de la plataforma.

High-Frequency Trading Architecture: A visualization of a C++ algorithmic bot digesting high-speed FIX/FAST network data streams.

Hello, friends! Today, I'll show you how to build your first trading scalper bot in C++ using the FAST/FIX protocols. Many believe that algorithmic trading is something extremely complex, accessible only to elite programmers with hedge fund experience. But let's be honest: you can start small, especially if you already have access to an exchange via FAST/FIX.

What Do We Need?

Before we dive into the code, let's prepare our toolkit:

C++ compiler (GCC, Clang, or MSVC)

Library for working with FIX/FAST (e.g., OnixS C++ FIX Engine)

A convenient IDE (Visual Studio, CLion, or your favorite)

A cup of strong coffee (optional, but highly recommended)

Understanding FIX/FAST Protocols

If you already have access to an exchange via FAST/FIX, you probably know that:

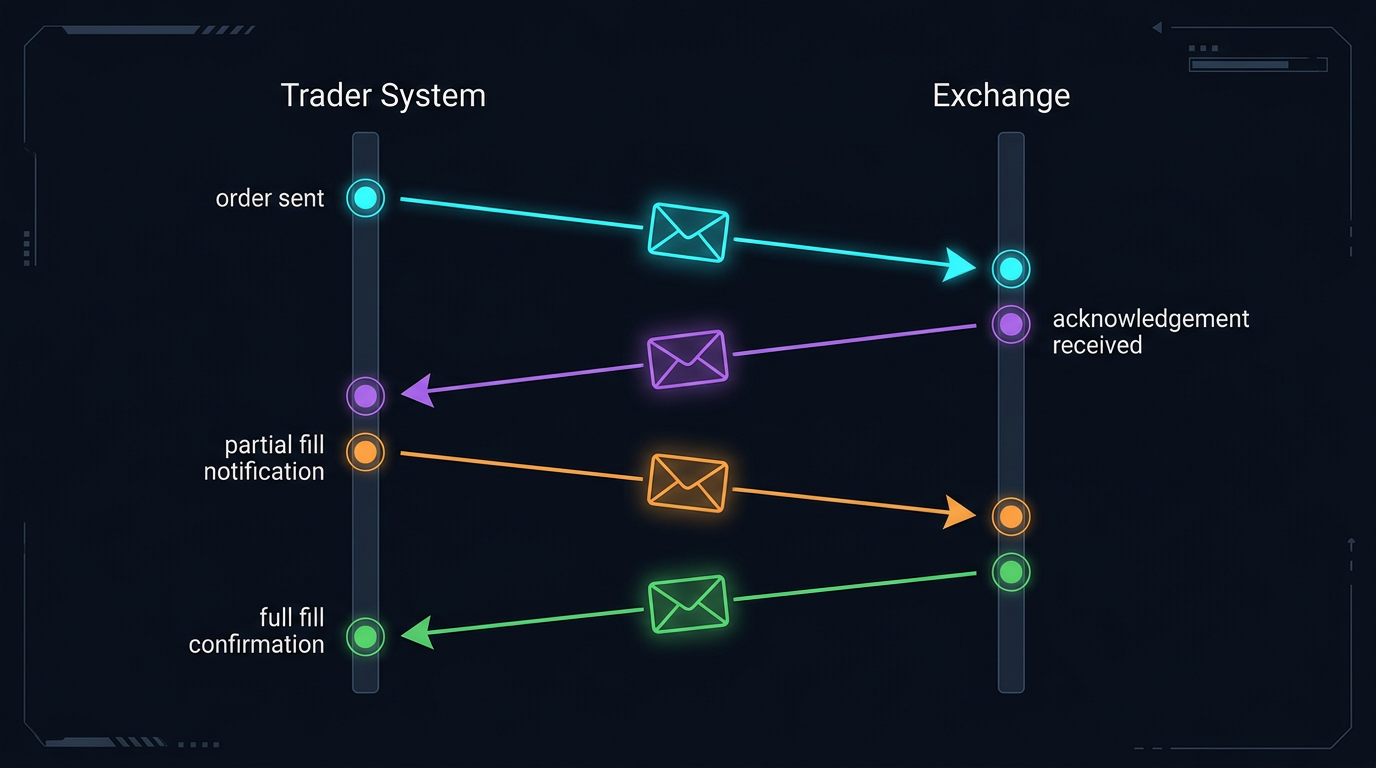

FIX (Financial Information eXchange) is a standard protocol for exchanging financial information. Imagine telegrams like "BUY BTCUSD QTY=1 PRICE=50000", but in a more formalized format.

FAST (FIX Adapted for Streaming) is a "turbo version" of FIX, optimized for high-speed data transfer. If FIX is regular mail, FAST is pneumatic mail on steroids.

Our Scalper's Architecture

Any self-respecting scalper should have the following components:

Exchange connection module – our bridge to the world of big money

Market data processing module – our "eyes and ears"

For simplicity, let's implement an RSI indicator and basic entry/exit logic:

doublecalculateRSI(const std::vector<double>& prices, int period = 14){

if (prices.size() < period + 1) return50.0;

double sumGain = 0.0, sumLoss = 0.0;

for (size_t i = prices.size() - period; i < prices.size() - 1; ++i) {

double change = prices[i + 1] - prices[i];

if (change > 0) sumGain += change;

else sumLoss -= change;

}

if (sumLoss == 0) return100.0;

double rs = sumGain / sumLoss;

return100.0 - (100.0 / (1.0 + rs));

}

Sending Orders to the Exchange

When our strategy says "buy" or "sell", we need to send the corresponding order to the exchange. It's like placing an order at a restaurant – you need to be precise:

voidSimpleScalper::sendBuyOrder(double amount, double price){

std::cout << "Sending BUY order: " << amount << " @ " << price << std::endl;

// Here we form and send a FIX NewOrderSingle// ...

}

Before running our bot with real money, let's test it on historical data or in simulation mode. This is like a pilot training on a simulator before a real flight:

That's it! We've built a simple yet functional C++ scalper using FAST/FIX protocols. Of course, this is just the beginning. Real HFT systems are much more complex and optimized, but even such a simple bot can be useful for a beginner algorithmic trader.

Remember, trading on financial markets involves risks, and algorithmic trading adds technical risks on top. Always test your strategies on historical data and in simulation mode before going live.

And most importantly – keep learning and improving your bot. Markets change, and your algorithms must adapt with them.

Happy trading, and may your scalper always be profitable!

Citation

@software{soloviov2024scalpercppfastfix,

author = {Soloviov, Eugen},

title = {Developing a Simple C++ Scalper Using FAST/FIX: Step-by-Step Guide},

year = {2025},

url = {https://marketmaker.cc/en/blog/post/scalper-cpp-fast-fix},

version = {0.1.0},

description = {A step-by-step guide to building a C++ trading scalper bot using FAST/FIX protocols.}

}

High-Frequency Trading Architecture: A visualization of a C++ algorithmic bot digesting high-speed FIX/FAST network data streams.

High-Frequency Trading Architecture: A visualization of a C++ algorithmic bot digesting high-speed FIX/FAST network data streams.