Suscríbete a nuestro boletín para recibir información exclusiva sobre trading con IA, análisis de mercado y actualizaciones de la plataforma.

Instead of a Preface: When Classical Machine Learning Gives Up

Cryptocurrency markets are where traditional forecasting methods come to die. LSTM models start getting nervous from Bitcoin's volatility, ARIMA models have hysterics from Ethereum's sharp jumps, and classical neural networks simply give up when they see Dogecoin's chart. And then diffusion models take the stage — technology that originally taught computers to draw cats, and now tries to predict when Bitcoin will decide to have another "Black Monday".

Funny enough, the architecture that gave birth to Stable Diffusion and DALL-E is now actively applied to financial time series analysis. And you know what? It works quite well. Especially when classical approaches start hallucinating from extreme cryptocurrency volatility.

Chaos to Clarity: How diffusion models extract structured signals from the high-noise environment of cryptocurrency markets

Why Do Diffusion Models Work with Time Series at All?

Diffusion models are a class of generative models that learn to restore original data from noise through a process of sequential "denoising". The basic idea is simple: we take real data, gradually add Gaussian noise to it until we get pure noise, and then teach a neural network to reverse this process.

In the context of financial time series, this means the model learns to separate signal from noise in the literal sense. Cryptocurrency markets are known for their extreme noisiness — random Elon Musk tweets, panic selling, FOMO buying. A diffusion model can learn to "see" structural patterns through all this chaos.

This is the flagship library for working with diffusion models for time series, published at ICLR 2024. The main advantage is that it works both conditionally (forecasting) and unconditionally (generation).

The model uses an encoder-decoder transformer with separated temporal representations, where decomposition helps capture the semantic meaning of time series.

2. TSDiff: Amazon's Approach to Cryptocurrency Chaos

Amazon Research proposed TSDiff — an unconditional diffusion model that can work with forecasting through a self-guidance mechanism. The peculiarity is that the model doesn't require additional networks for conditioning.

For those who want to quickly try diffusion models in combination with proven architectures:

import lightning.pytorch as pl

from pytorch_forecasting import TimeSeriesDataSet, TemporalFusionTransformer

from diffusion_wrapper import DiffusionTFT # hypothetical wrapper

crypto_df = pd.read_csv('hourly_crypto_data.csv')

training = TimeSeriesDataSet(

crypto_df,

time_idx="hour",

target="btc_price",

group_ids=["crypto_pair"],

max_encoder_length=168, # week back

max_prediction_length=24, # day forward

time_varying_unknown_reals=["price", "volume", "volatility"],

time_varying_known_reals=["hour_of_day", "day_of_week"],

)

diffusion_tft = DiffusionTFT.from_dataset(

training,

hidden_size=64,

attention_head_size=4,

diffusion_steps=100,

noise_schedule='linear'

)

trainer = pl.Trainer(max_epochs=50, accelerator="gpu")

trainer.fit(diffusion_tft, train_dataloaders=training.to_dataloader(train=True))

Practical Results: Diffusion vs Classics

Research shows curious results. In the paper "Prediction of Cryptocurrency Prices through a Path Dependent Monte Carlo Simulation", authors use Merton's jump diffusion model — a hybrid of stochastic processes and machine learning. The result? The model was able to capture both gradual price changes and sharp jumps characteristic of cryptocurrency markets.

Another study showed that ADE-TFT (Advanced Deep Learning-Enhanced Temporal Fusion Transformer) with diffusion components significantly outperforms classical approaches in MAPE, MSE, and RMSE metrics. Results on the 8-hidden-layer configuration are especially impressive.

Probabilistic Forecasting: Using diffusion models to generate future price paths with associated confidence intervals

The Dark Side of Diffusion Models in Finance

But let's be honest. Diffusion models are not a silver bullet. They have serious problems:

1. Computational Greediness

Training a diffusion model on cryptocurrency data requires serious computational resources. If your model makes 1000 diffusion steps, then to get one forecast you need 1000 passes through the neural network. This isn't very suitable for high-frequency trading.

2. Black Swan Problem

Cryptocurrency markets are known for extreme events — 50% crash in a day, cryptocurrency ban in China, major exchange hack. Diffusion models trained on historical data poorly predict such events.

3. Regime Dependence

Cryptocurrency markets have various behavioral regimes — bull market, bear market, sideways movement. A diffusion model can work excellently in one regime and completely fail in another.

Optimization and Acceleration: How Not to Go Bankrupt on GPU

You have lots of historical data (minimum one year of hourly data)

You can afford long training (days-weeks on GPU)

Need synthetic scenario generation for backtesting

Working with multivariate time series

Uncertainty estimation of forecasts is important

Not worth using if:

Need fast forecasts in real-time

Working with short time series

Limited computational resources

Model interpretability is critical

The Future of Diffusion Models in Crypto Analytics

Diffusion models in finance are like cryptocurrencies in 2010. The technology is raw, resource-intensive, but the potential is enormous. We already see hybrid approaches: DDPM + Transformer, diffusion + reinforcement learning, conditional diffusion for market regimes.

The next breakthrough is expected in multimodal diffusion — models that will consider not only prices but also news, social signals, on-chain metrics. Imagine a diffusion model that "sees" the correlation between Elon Musk's tweet and Dogecoin movement.

Conclusion: Diffusion as Evolution, Not Revolution

Diffusion models won't replace classical approaches to cryptocurrency forecasting. They will complement them. LSTM will remain for fast forecasts, ARIMA — for stationary sections, and diffusion will take on scenario generation and work with extreme volatility.

The main lesson: in the world of cryptocurrencies, there are no silver bullets. There's only smart combination of tools, deep market understanding, and healthy skepticism towards any "revolutionary" solutions. Diffusion models are a powerful tool, but remember: they're just trying to find patterns in chaos. And chaos, as we know, doesn't really like being predicted.

P.S.: If your diffusion model shows 95% accuracy on Bitcoin forecasting — check the code twice. Most likely, there's data leakage somewhere 😉

Chaos to Clarity: How diffusion models extract structured signals from the high-noise environment of cryptocurrency markets

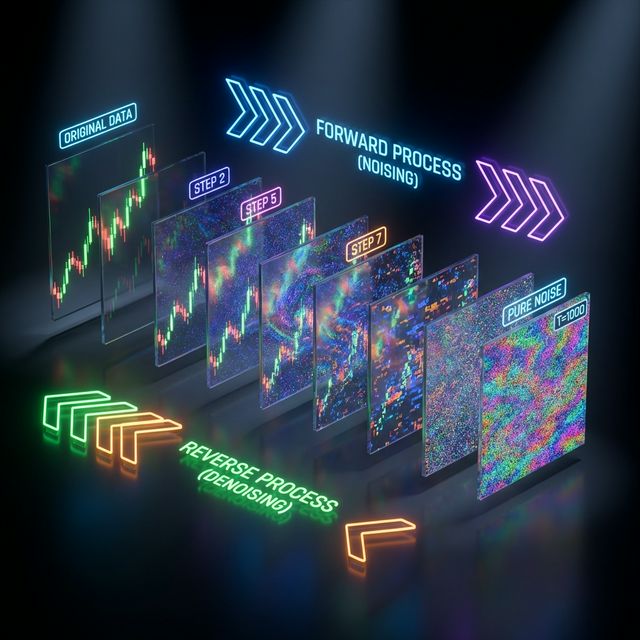

Chaos to Clarity: How diffusion models extract structured signals from the high-noise environment of cryptocurrency markets Sequential Denoising: The forward process (adding noise) and reverse process (denoising) to reconstruct financial time series

Sequential Denoising: The forward process (adding noise) and reverse process (denoising) to reconstruct financial time series Probabilistic Forecasting: Using diffusion models to generate future price paths with associated confidence intervals

Probabilistic Forecasting: Using diffusion models to generate future price paths with associated confidence intervals