Assine nossa newsletter para insights exclusivos sobre trading com IA, análises de mercado e atualizações da plataforma.

Minute candles are the standard granularity for backtests. But within a single minute candle, price can move differently: sometimes by 0.01%, other times by 2%. When both stop-loss and take-profit fall within the [low, high] range of a single minute candle, the backtest doesn't know which triggered first. This is the fill ambiguity problem.

The naive solution is to switch to second-level data for the entire backtest. But over two years, that's ~63 million second bars instead of ~1 million minute bars. Storage increases 60x, speed drops proportionally.

Adaptive drill-down solves this problem: use fine granularity only where it's actually needed.

The Problem: Fill Ambiguity on Large Candles

Consider a specific situation. The strategy opened a long at 3000 USDT. Stop-loss: 2970 (-1%). Take-profit: 3060 (+2%).

The minute candle at 14:37:

Open: 3010

High: 3065

Low: 2965

Close: 3050

Both SL (2970) and TP (3060) fall within the range [2965, 3065]. Which triggered first?

Possible outcomes:

Price went down first -> SL triggered -> loss of -1%

Price went up first -> TP triggered -> profit of +2%

The difference in a single trade: 3 percentage points. With 10x leverage — 30%. For a backtest with hundreds of trades, incorrect fill ambiguity resolution systematically distorts results.

How Frameworks Handle This by Default

Most backtest engines use one of two heuristics:

Optimistic: TP triggers first -> inflated results

Pessimistic: SL triggers first -> deflated results

Both approaches are guesswork. Real data is available at second or even millisecond level, and there's no reason to guess when you can look.

Drill-Down: Three-Level Strategy

The drill-down idea: start at the minute level and "drill down" to a lower level only when there's ambiguity.

Level 1: 1m (minute candles)

-> If SL or TP is unambiguously outside the [low, high] range — resolve on the spot

-> If both are within the range — drill down

Level 2: 1s (second candles)

-> Load 60 second bars for this minute

-> Walk through second by second: which triggered first?

-> If a second bar is also ambiguous — drill down

Level 3: 100ms (millisecond candles)

-> Load up to 10 bars of 100ms for this second

-> Resolve the fill at order book level

When Drill-Down Is Not Needed

In 95% of cases, drill-down is not required. Typical scenarios:

Unambiguous SL: candle high doesn't reach TP, low breaks through SL -> SL triggered, no drill-down needed.

Unambiguous TP: low doesn't reach SL, high breaks through TP -> TP triggered, no drill-down needed.

Neither triggered: both levels are outside the range -> position remains open.

Gap detection: the open of the next candle jumps through SL or TP -> execution at open price, no drill-down.

Drill-down is needed only for ~5% of bars — when both levels fall within the range of a single candle.

classAdaptiveFillSimulator:

"""

Three-level drill-down for determining fill order.

"""def__init__(self, data_loader):

self.loader = data_loader

self.cache_1s = {} # Cache of second data by monthdefcheck_fill(self, timestamp, candle_1m, sl_price, tp_price, side):

"""

Checks whether SL or TP triggered on the given minute candle.

Returns: ('sl', fill_price) | ('tp', fill_price) | None

"""

low, high = candle_1m['low'], candle_1m['high']

open_price = candle_1m['open']

if side == 'long':

if open_price <= sl_price:

return ('sl', open_price)

if open_price >= tp_price:

return ('tp', open_price)

else:

if open_price >= sl_price:

return ('sl', open_price)

if open_price <= tp_price:

return ('tp', open_price)

sl_hit = self._level_hit(sl_price, low, high, side, 'sl')

tp_hit = self._level_hit(tp_price, low, high, side, 'tp')

if sl_hit andnot tp_hit:

return ('sl', sl_price)

if tp_hit andnot sl_hit:

return ('tp', tp_price)

ifnot sl_hit andnot tp_hit:

returnNonereturnself._drill_down_1s(timestamp, sl_price, tp_price, side)

def_drill_down_1s(self, minute_ts, sl_price, tp_price, side):

"""Level 2: second-by-second pass."""

bars_1s = self.loader.load_1s_for_minute(minute_ts)

if bars_1s isNoneorlen(bars_1s) == 0:

returnself._pessimistic_fill(side, sl_price, tp_price)

for bar in bars_1s:

sl_hit = self._level_hit(sl_price, bar['low'], bar['high'], side, 'sl')

tp_hit = self._level_hit(tp_price, bar['low'], bar['high'], side, 'tp')

if sl_hit andnot tp_hit:

return ('sl', sl_price)

if tp_hit andnot sl_hit:

return ('tp', tp_price)

if sl_hit and tp_hit:

result = self._drill_down_100ms(bar['timestamp'], sl_price, tp_price, side)

if result:

return result

returnself._pessimistic_fill(side, sl_price, tp_price)

def_pessimistic_fill(self, side, sl_price, tp_price):

"""Pessimistic assumption: SL for longs, TP for shorts."""if side == 'long':

return ('sl', sl_price)

else:

return ('sl', sl_price)

Performance

Mode

Time per fill check

When used

1m (no drill-down)

~0ms

~95% of cases

1s drill-down

~5ms (first access to month)

~5% of cases

100ms drill-down

~1ms

<0.5% of cases

Over a 2-year backtest with ~400 trades, drill-down is invoked for approximately 20 candles. Total overhead — less than 1 second for the entire backtest.

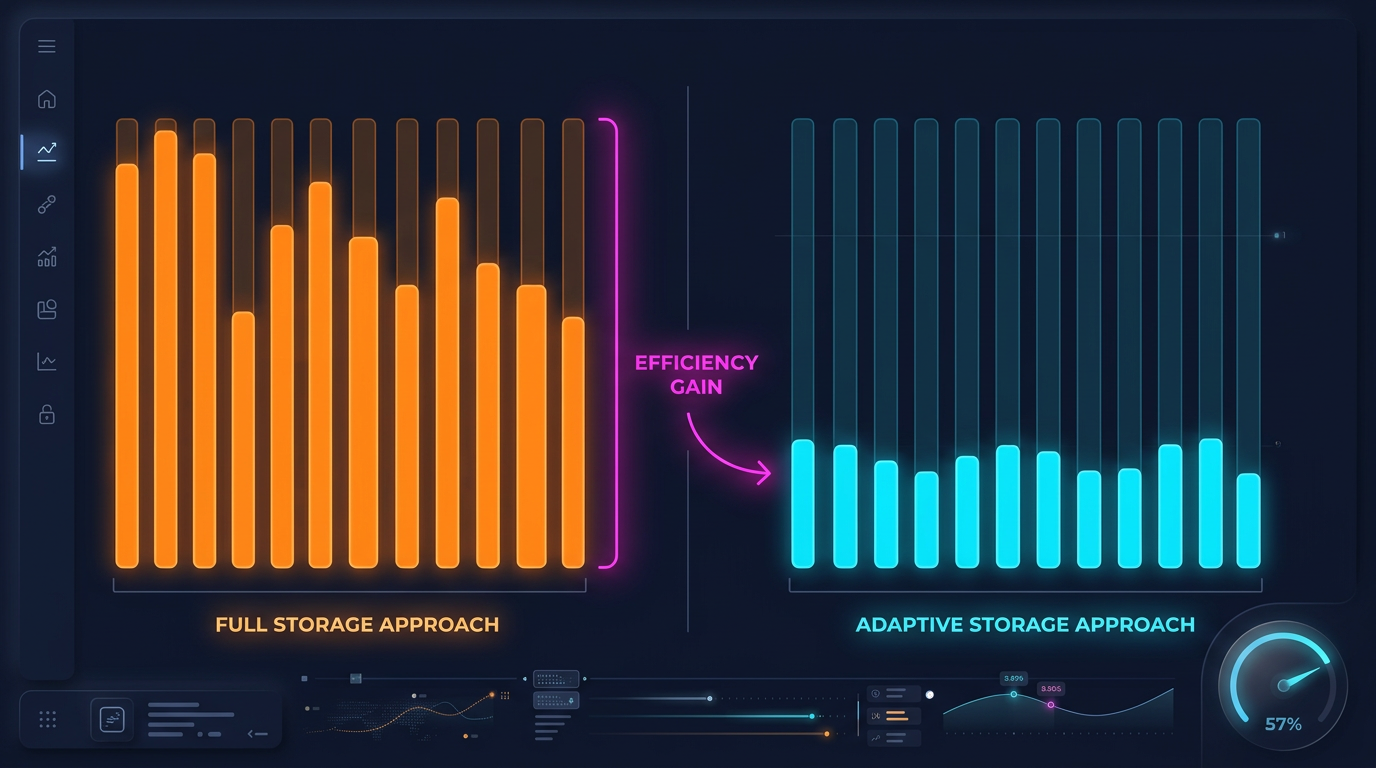

Adaptive Data Storage

Drill-down requires second and millisecond data. But storing everything at maximum granularity is impractical:

Granularity

Bars over 2 years

Parquet size

1m

~1.05M

~15 MB

1s

~63M

~550 MB/month

100ms

~630M

~5 GB/month

A complete 1s archive over 2 years is about 13 GB. 100ms — over 100 GB. Storing everything is possible but wasteful, considering that drill-down uses less than 1% of this data.

Hot-Second Detection

The key observation: seconds in which price moves significantly represent a small fraction. If price changed by less than 0.1% within a second — there's no point storing the 100ms breakdown for that second.

Hot-second detection: when downloading and processing data, we analyze each second and generate 100ms candles only for "hot" seconds — those where price movement exceeded the threshold.

defprocess_trades_adaptive(

trades: pd.DataFrame,

min_price_change_pct: float = 1.0,

) -> tuple[pd.DataFrame, pd.DataFrame]:

"""

Processes raw trades into an adaptive structure:

- 1s candles for all seconds

- 100ms candles only for "hot" seconds

Args:

trades: DataFrame with columns [timestamp, price, quantity]

min_price_change_pct: threshold for drill-down to 100ms

Returns:

(df_1s, df_100ms_hot) — second candles and 100ms for hot seconds

"""

trades['second'] = trades['timestamp'].dt.floor('1s')

df_1s = trades.groupby('second').agg(

open=('price', 'first'),

high=('price', 'max'),

low=('price', 'min'),

close=('price', 'last'),

volume=('quantity', 'sum'),

)

df_1s['price_change_pct'] = (df_1s['high'] - df_1s['low']) / df_1s['open'] * 100

hot_seconds = df_1s[df_1s['price_change_pct'] >= min_price_change_pct].index

hot_trades = trades[trades['second'].isin(hot_seconds)]

hot_trades['bucket_100ms'] = hot_trades['timestamp'].dt.floor('100ms')

df_100ms = hot_trades.groupby('bucket_100ms').agg(

open=('price', 'first'),

high=('price', 'max'),

low=('price', 'min'),

close=('price', 'last'),

volume=('quantity', 'sum'),

)

return df_1s, df_100ms

Storage Savings

For example — ETHUSDT over a typical month:

Approach

Size

Granularity

1m only

~1 MB

1 minute

All 1s

~550 MB

1 second

All 100ms

~5 GB

100 ms

Adaptive

~600 MB

1s + 100ms only for hot seconds

With a threshold of min_price_change_pct = 1.0%, hot seconds account for less than 1% of all seconds. 100ms data for them adds ~50 MB to the 550 MB of second data — a negligible overhead.

If second data is also stored adaptively (only when movement within a minute exceeds 0.1%), the volume can be reduced by another 3-5x.

DELTA_BINARY_PACKED for timestamps: consecutive timestamps differ by a fixed value (60 for 1m, 1 for 1s). Delta encoding compresses them to nearly zero.

BYTE_STREAM_SPLIT for float: splits float32 bytes into streams (all first bytes together, all second bytes together, etc.). For smoothly changing prices, this achieves 2-3x better compression than standard encoding.

ZSTD level 9: good compression with acceptable decompression speed.

float32 instead of float64: sufficient for prices and volumes, saves 50% memory.

Lazy Loading with Caching

Drill-down requests second data for a specific minute. Loading a parquet file for each request is slow. The solution — lazy loading with an LRU cache by month.

from functools import lru_cache

import pyarrow.parquet as pq

import pandas as pd

classAdaptiveDataLoader:

"""

Lazy loader with cache: loads second data by month,

keeps the last N months in memory.

"""def__init__(self, symbol: str, data_dir: str = "data", cache_months: int = 2):

self.symbol = symbol

self.data_dir = data_dir

self.cache_months = cache_months

self._cache_1s: dict[str, pd.DataFrame] = {}

defload_1s_for_minute(self, minute_ts: pd.Timestamp) -> pd.DataFrame | None:

"""Load 1s data for a specific minute."""

month_key = minute_ts.strftime("%Y-%m")

if month_key notinself._cache_1s:

self._load_month_1s(month_key)

if month_key notinself._cache_1s:

returnNone

df = self._cache_1s[month_key]

minute_start = minute_ts.floor('1min')

minute_end = minute_start + pd.Timedelta(minutes=1)

return df[(df.index >= minute_start) & (df.index < minute_end)]

defload_100ms_for_second(self, second_ts: pd.Timestamp) -> pd.DataFrame | None:

"""Load 100ms data for a hot second."""

month_key = second_ts.strftime("%Y-%m")

path = f"{self.data_dir}/{self.symbol}/klines_100ms_hot/{month_key}.parquet"try:

df = pd.read_parquet(path)

second_start = second_ts.floor('1s')

second_end = second_start + pd.Timedelta(seconds=1)

return df[(df.index >= second_start) & (df.index < second_end)]

except FileNotFoundError:

returnNonedef_load_month_1s(self, month_key: str):

"""Load a month of 1s data, evict old data from cache."""

path = f"{self.data_dir}/{self.symbol}/klines_1s/{month_key}.parquet"try:

df = pd.read_parquet(path)

df.index = pd.to_datetime(df['timestamp'], unit='s')

iflen(self._cache_1s) >= self.cache_months:

oldest = min(self._cache_1s.keys())

delself._cache_1s[oldest]

self._cache_1s[month_key] = df

except FileNotFoundError:

pass

Applying Drill-Down to Backtesting

Integration into the backtest loop:

defbacktest_with_adaptive_fill(

states: pd.DataFrame,

strategy_params: dict,

data_loader: AdaptiveDataLoader,

) -> list:

"""

Backtest with adaptive drill-down for fill simulation.

"""

fill_sim = AdaptiveFillSimulator(data_loader)

trades = []

position = Nonefor i inrange(len(states)):

row = states.iloc[i]

ts = states.index[i]

candle_1m = {

'open': row['open'], 'high': row['high'],

'low': row['low'], 'close': row['close'],

'timestamp': ts,

}

if position isnotNone:

fill = fill_sim.check_fill(

ts, candle_1m,

position['sl'], position['tp'],

position['side'],

)

if fill isnotNone:

fill_type, fill_price = fill

trades.append({

'entry_time': position['entry_time'],

'exit_time': ts,

'side': position['side'],

'entry_price': position['entry_price'],

'exit_price': fill_price,

'exit_type': fill_type,

'drill_down': fill_sim.last_drill_depth, # 0, 1, or 2

})

position = Nonecontinue

signal = check_entry_signal(row, strategy_params)

if signal and position isNone:

position = {

'side': signal['side'],

'entry_price': row['close'],

'entry_time': ts,

'sl': signal['sl'],

'tp': signal['tp'],

}

return trades

Both approaches eliminate errors invisible at the daily candle level but critical for realistic backtesting.

Summary: Fill Simulation Approach Comparison

Approach

Accuracy

Speed

Storage

OHLC heuristic (optimist/pessimist)

Low

Instant

1m only

Full 1s backtest

High

Slow (x60)

~550 MB/month

Full 100ms backtest

Maximum

Very slow (x600)

~5 GB/month

Adaptive drill-down

High

~Instant

1m + 1s + 100ms hot

Drill-down provides the accuracy of a full 1s backtest at the speed of a 1m backtest. The key observation: high granularity is not needed everywhere — only at decision points.

Conclusion

Adaptive drill-down is the application of a simple principle: spend computational resources and storage proportionally to data importance.

Three granularity levels:

1m — base pass for 95% of bars

1s — drill-down during fill ambiguity

100ms — drill-down for hot seconds with extreme movement

Three storage levels:

All 1m — complete archive, ~15 MB for 2 years

All 1s — complete or adaptive archive, ~550 MB/month

Hot 100ms only — <1% of seconds, ~50 MB/month

The result: a backtest with tick simulator accuracy at minute-level speed. And storage that grows linearly, not exponentially, with increasing granularity.

@article{soloviov2026adaptivedrilldown,

author = {Soloviov, Eugen},

title = {Adaptive Drill-Down: Backtest with Variable Granularity from Minutes to Milliseconds},

year = {2026},

url = {https://marketmaker.cc/ru/blog/post/adaptive-resolution-drill-down-backtest},

description = {How adaptive data granularity speeds up backtests and saves storage: drill-down from 1m to 1s and 100ms only where price moved significantly.}

}