뉴스레터를 구독하여 독점적인 AI 트레이딩 통찰력, 시장 분석 및 플랫폼 업데이트를 받아보세요.

The "desire orderbook" represents a revolutionary concept in market structure analysis, based on predicting potential actions of market participants before their actual execution. Unlike a standard orderbook that reflects current buy and sell orders, the "desire orderbook" is built on assumptions about traders' future intentions.

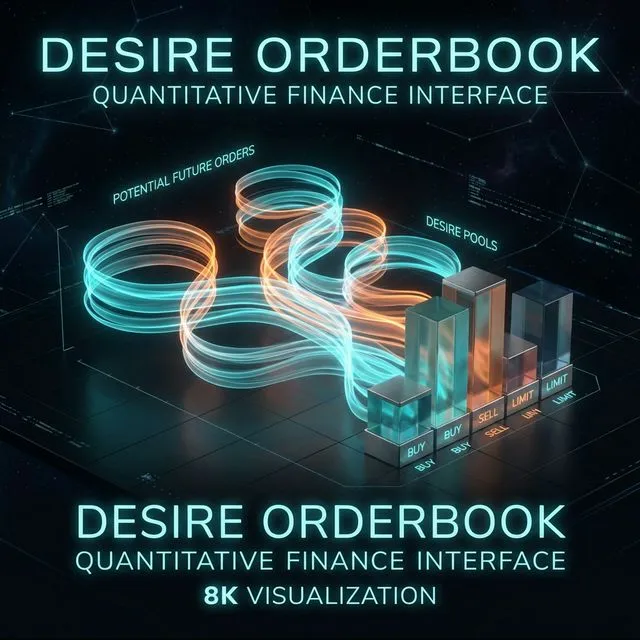

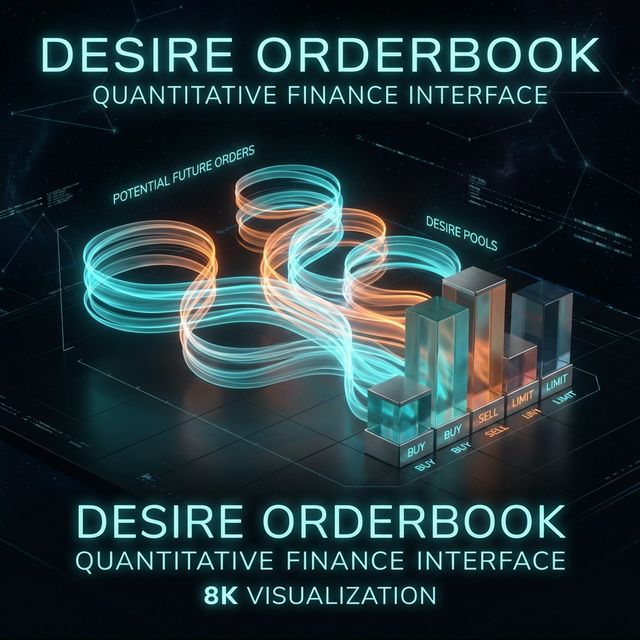

The Desire Orderbook Concept: Abstract gradients of potential future orders crystallizing into solid market liquidity structure.

Theoretical Foundation of the Concept

The "desire orderbook" concept is based on the assumption that most traders have an internal model of targeted position realization, which is often not reflected in current market orders. This model assumes that traders:

Enter positions with a specific exit plan

Have flexible realization strategies depending on market conditions

Are psychologically attached to certain price levels (round numbers, entry levels, breakeven points)

Tend to distribute the realization of large positions through a series of smaller orders

Gradient Approach to Order Modeling

The key innovation of the concept lies in presenting each potential order not as a point event, but as a gradient or "ladder" of probabilities:

Solution: use of distributed computing, optimized aggregation algorithms

User privacy - detailed behavior analysis may raise privacy concerns

Solution: data anonymization, aggregation at the level of user groups

Dynamic updating - market conditions and trader intentions change rapidly

Solution: incremental model updating in real-time

Visualization of the Desire Orderbook

Visualization of the "desire orderbook" can take various forms:

Heat map - color intensity reflects the probability of orders appearing at a given price level

Volume profile - three-dimensional representation where the third dimension is probability

Gradient ribbon - continuous gradient showing smooth probability changes

Market Liquidity Heat Map: Red zones indicate a high probability of sell walls forming based on predictive models.

Conclusion

The "desire orderbook" concept represents a revolutionary approach to market structure analysis, especially in the context of decentralized finance. The transition from a deterministic orderbook to a probabilistic one allows for a substantially expanded understanding of potential market dynamics.

By representing orders not as point events but as probability gradients, this model more accurately reflects real trader behavior, who often distribute their buy or sell decisions across various price levels. The overlay of thousands of such gradients creates a multidimensional map of potential market activity, revealing hidden levels of support and resistance.

In an era where data is becoming the new oil, the "desire orderbook" concept represents an innovative way to extract valuable insights from existing blockchain data, potentially revolutionizing approaches to market analysis and trading strategies.

Citation

@software{soloviov2025desireorderbook,

author = {Soloviov, Eugen},

title = {The 'Desire Orderbook' Concept: An Innovative Approach to Market Behavior Prediction},

year = {2025},

url = {https://marketmaker.cc/en/blog/post/desire-orderbook},

version = {0.1.0},

description = {Desire orderbook — a revolutionary concept of market structure analysis based on predicting potential actions of market participants before their actual execution.}

}

The Desire Orderbook Concept: Abstract gradients of potential future orders crystallizing into solid market liquidity structure.

The Desire Orderbook Concept: Abstract gradients of potential future orders crystallizing into solid market liquidity structure. Probability Gradients: Visualizing the increasing likelihood of execution as price approaches a trader's psychological threshold.

Probability Gradients: Visualizing the increasing likelihood of execution as price approaches a trader's psychological threshold. Market Liquidity Heat Map: Red zones indicate a high probability of sell walls forming based on predictive models.

Market Liquidity Heat Map: Red zones indicate a high probability of sell walls forming based on predictive models.