AI сауда талдаулары, нарық аналитикасы және платформа жаңалықтары үшін біздің ақпараттық бюллетеньге жазылыңыз.

The Distance Approach in pairs trading has gained significant popularity due to its elegant simplicity and effectiveness. This technique identifies asset pairs through statistical measures and trades based on the divergence and convergence of their price relationships. This article provides a comprehensive analysis of both basic and advanced Distance Approach methodologies, with practical implementations in Rust tailored for high-frequency traders, algorithmic developers, mathematicians, and programmers seeking robust solutions.

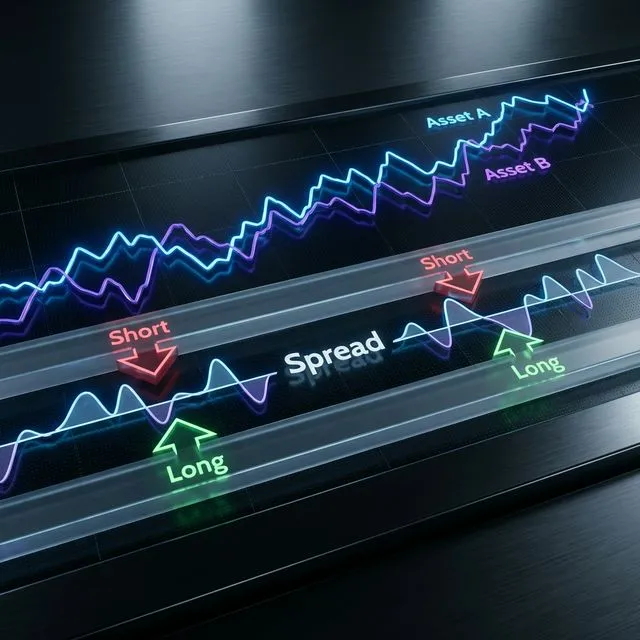

Visualizing the Distance Approach: Assets A and B tracking each other, with trading signals generated based on spread divergence (Long/Short)

Theoretical Foundation of the Distance Approach

The Distance Approach establishes a framework for pairs trading based on normalized price movements between assets. At its core, the method uses Euclidean squared distance measurements to identify assets that historically move together and generates trading signals when their normalized price divergence exceeds statistically significant thresholds[2].

This approach consists of two primary stages:

Pairs formation - identifying statistically related asset pairs

Trading signal generation - creating entry and exit rules based on divergence

Mathematical Basis

The basic implementation utilizes Euclidean distance between normalized price series. For two assets with normalized price time series X and Y, we calculate:

fneuclidean_squared_distance(x: &[f64], y: &[f64]) ->f64 {

assert_eq!(x.len(), y.len(), "Time series must have equal length");

x.iter()

.zip(y.iter())

.map(|(xi, yi)| (xi - yi).powi(2))

.sum()

}

This distance metric helps identify assets that historically move together, providing the foundation for statistical arbitrage opportunities[2].

Basic Distance Approach Implementation

Data Normalization

Before calculating distances, we must normalize price data to establish comparable scales. Min-max normalization is commonly applied:

The Pearson Correlation approach offers several advantages over the basic Distance Approach, focusing on return correlations rather than price distances[1].

Implementation in Rust

fnpearson_correlation(x: &[f64], y: &[f64]) ->f64 {

assert_eq!(x.len(), y.len(), "Arrays must have the same length");

letn = x.len() asf64;

letsum_x: f64 = x.iter().sum();

letsum_y: f64 = y.iter().sum();

letsum_xx: f64 = x.iter().map(|&val| val * val).sum();

letsum_yy: f64 = y.iter().map(|&val| val * val).sum();

letsum_xy: f64 = x.iter().zip(y.iter()).map(|(&xi, &yi)| xi * yi).sum();

letnumerator = n * sum_xy - sum_x * sum_y;

letdenominator = ((n * sum_xx - sum_x * sum_x) * (n * sum_yy - sum_y * sum_y)).sqrt();

if denominator.abs() < f64::EPSILON {

return0.0;

}

numerator / denominator

}

structPearsonPair {

stock_idx: usize,

comover_indices: Vec<usize>,

correlations: Vec<f64>,

}

fnfind_pearson_pairs(returns: &[Vec<f64>], top_n_comovers: usize) ->Vec<PearsonPair> {

letstock_count = returns.len();

letmut all_pairs = Vec::new();

foriin0..stock_count {

letmut correlations = Vec::with_capacity(stock_count - 1);

forjin0..stock_count {

if i == j {

continue;

}

letcorrelation = pearson_correlation(&returns[i], &returns[j]).abs();

correlations.push((j, correlation));

}

// Sort by correlation (highest first)

correlations.sort_by(|a, b| b.1.partial_cmp(&a.1).unwrap_or(std::cmp::Ordering::Equal));

// Take top N comoverslettop_comovers: Vec<(usize, f64)> = correlations.into_iter()

.take(top_n_comovers)

.collect();

let (comover_indices, correlation_values): (Vec<usize>, Vec<f64>) =

top_comovers.into_iter().unzip();

all_pairs.push(PearsonPair {

stock_idx: i,

comover_indices,

correlations: correlation_values,

});

}

all_pairs

}

Portfolio Formation and Beta Calculation

The Pearson approach creates portfolios of comovers for each stock, then calculates regression coefficients:

For integration testing, we would follow the Rust convention of placing tests in a separate tests directory at the project root[15][18].

Conclusion

The Distance Approach provides a robust framework for pairs trading, with both basic and

advanced methodologies offering valuable statistical arbitrage opportunities. The basic

approach, with its focus on Euclidean distance, offers simplicity and effectiveness, while

the Pearson Correlation approach provides additional flexibility and potentially better

divergence reversion characteristics.

Rust's performance characteristics make it an ideal language for implementing these

computationally intensive strategies, especially with optimizations like SIMD and

concurrent processing. The combination of statistical rigor and efficient implementation

creates a powerful toolkit for algorithmic traders.

When implementing a pairs trading system, several considerations should be made:

The trade-off between simplicity (basic approach) and enhanced statistical power

(Pearson approach)

The computational resources required for large-scale pair analysis

Transaction costs, which can significantly impact profitability[3]

The need for continuous monitoring and recalibration of pairs

By combining the Distance Approach with Rust's performance capabilities, traders can

develop highly efficient and effective statistical arbitrage systems capable of operating

at the speed and scale required for modern markets.

Citation

@software{soloviov2025distanceapproach,

author = {Soloviov, Eugen},

title = {Distance Approach in Pairs Trading: Implementation and Analysis with Rust},

year = {2025},

url = {https://marketmaker.cc/en/blog/post/distance-approach-pairs-trading},

version = {0.1.0},

description = {A comprehensive analysis of basic and advanced Distance Approach methodologies for pairs trading, with practical implementations in Rust tailored for high-frequency traders and algorithmic developers.}

}

Visualizing the Distance Approach: Assets A and B tracking each other, with trading signals generated based on spread divergence (Long/Short)

Visualizing the Distance Approach: Assets A and B tracking each other, with trading signals generated based on spread divergence (Long/Short) Zero-Crossings concept: identifying pairs that frequently mean-revert, indicated by the spread crossing the zero line

Zero-Crossings concept: identifying pairs that frequently mean-revert, indicated by the spread crossing the zero line SIMD acceleration: utilizing data-level parallelism in Rust to process multiple price points simultaneously, drastically reducing latency

SIMD acceleration: utilizing data-level parallelism in Rust to process multiple price points simultaneously, drastically reducing latency