Disclaimer: The information provided in this article is for educational and informational purposes only and does not constitute financial, investment, or trading advice. Trading cryptocurrencies involves significant risk of loss.

Subscribe to our newsletter for exclusive AI trading insights, market analysis, and platform updates.

Minute candles are the standard granularity for backtests. But within a single minute candle, price can move differently: sometimes by 0.01%, other times by 2%. When both stop-loss and take-profit fall within the [low, high] range of a single minute candle, the backtest doesn't know which triggered first. This is the fill ambiguity problem.

The naive solution is to switch to second-level data for the entire backtest. But over two years, that's ~63 million second bars instead of ~1 million minute bars. Storage increases 60x, speed drops proportionally.

Adaptive drill-down solves this problem: use fine granularity only where it's actually needed.

The Problem: Fill Ambiguity on Large Candles

Consider a specific situation. The strategy opened a long at 3000 USDT. Stop-loss: 2970 (-1%). Take-profit: 3060 (+2%).

The minute candle at 14:37:

Open: 3010

High: 3065

Low: 2965

Close: 3050

Both SL (2970) and TP (3060) fall within the range [2965, 3065]. Which triggered first?

Possible outcomes:

Price went down first -> SL triggered -> loss of -1%

Price went up first -> TP triggered -> profit of +2%

The difference in a single trade: 3 percentage points. With 10x leverage — 30%. For a backtest with hundreds of trades, incorrect fill ambiguity resolution systematically distorts results.

How Frameworks Handle This by Default

Most backtest engines use one of two heuristics:

Optimistic: TP triggers first -> inflated results

Pessimistic: SL triggers first -> deflated results

Both approaches are guesswork. Real data is available at second or even millisecond level, and there's no reason to guess when you can look.

Drill-Down: Three-Level Strategy

The drill-down idea: start at the minute level and "drill down" to a lower level only when there's ambiguity.

Level 1: 1m (minute candles)

-> If SL or TP is unambiguously outside the [low, high] range — resolve on the spot

-> If both are within the range — drill down

Level 2: 1s (second candles)

-> Load 60 second bars for this minute

-> Walk through second by second: which triggered first?

-> If a second bar is also ambiguous — drill down

Level 3: 100ms (millisecond candles)

-> Load up to 10 bars of 100ms for this second

-> Resolve the fill at order book level

When Drill-Down Is Not Needed

In 95% of cases, drill-down is not required. Typical scenarios:

Unambiguous SL: candle high doesn't reach TP, low breaks through SL -> SL triggered, no drill-down needed.

Unambiguous TP: low doesn't reach SL, high breaks through TP -> TP triggered, no drill-down needed.

Neither triggered: both levels are outside the range -> position remains open.

Gap detection: the open of the next candle jumps through SL or TP -> execution at open price, no drill-down.

Drill-down is needed only for ~5% of bars — when both levels fall within the range of a single candle.

classAdaptiveFillSimulator:

"""

Three-level drill-down for determining fill order.

"""def__init__(self, data_loader):

self.loader = data_loader

self.cache_1s = {} # Cache of second data by monthdefcheck_fill(self, timestamp, candle_1m, sl_price, tp_price, side):

"""

Checks whether SL or TP triggered on the given minute candle.

Returns: ('sl', fill_price) | ('tp', fill_price) | None

"""

low, high = candle_1m['low'], candle_1m['high']

open_price = candle_1m['open']

if side == 'long':

if open_price <= sl_price:

return ('sl', open_price)

if open_price >= tp_price:

return ('tp', open_price)

else:

if open_price >= sl_price:

return ('sl', open_price)

if open_price <= tp_price:

return ('tp', open_price)

sl_hit = self._level_hit(sl_price, low, high, side, 'sl')

tp_hit = self._level_hit(tp_price, low, high, side, 'tp')

if sl_hit andnot tp_hit:

return ('sl', sl_price)

if tp_hit andnot sl_hit:

return ('tp', tp_price)

ifnot sl_hit andnot tp_hit:

returnNonereturnself._drill_down_1s(timestamp, sl_price, tp_price, side)

def_drill_down_1s(self, minute_ts, sl_price, tp_price, side):

"""Level 2: second-by-second pass."""

bars_1s = self.loader.load_1s_for_minute(minute_ts)

if bars_1s isNoneorlen(bars_1s) == 0:

returnself._pessimistic_fill(side, sl_price, tp_price)

for bar in bars_1s:

sl_hit = self._level_hit(sl_price, bar['low'], bar['high'], side, 'sl')

tp_hit = self._level_hit(tp_price, bar['low'], bar['high'], side, 'tp')

if sl_hit andnot tp_hit:

return ('sl', sl_price)

if tp_hit andnot sl_hit:

return ('tp', tp_price)

if sl_hit and tp_hit:

result = self._drill_down_100ms(bar['timestamp'], sl_price, tp_price, side)

if result:

return result

returnself._pessimistic_fill(side, sl_price, tp_price)

def_pessimistic_fill(self, side, sl_price, tp_price):

"""Pessimistic assumption: SL for longs, TP for shorts."""if side == 'long':

return ('sl', sl_price)

else:

return ('sl', sl_price)

Performance

Mode

Time per fill check

When used

1m (no drill-down)

~0ms

~95% of cases

1s drill-down

~5ms (first access to month)

~5% of cases

100ms drill-down

~1ms

<0.5% of cases

Over a 2-year backtest with ~400 trades, drill-down is invoked for approximately 20 candles. Total overhead — less than 1 second for the entire backtest.

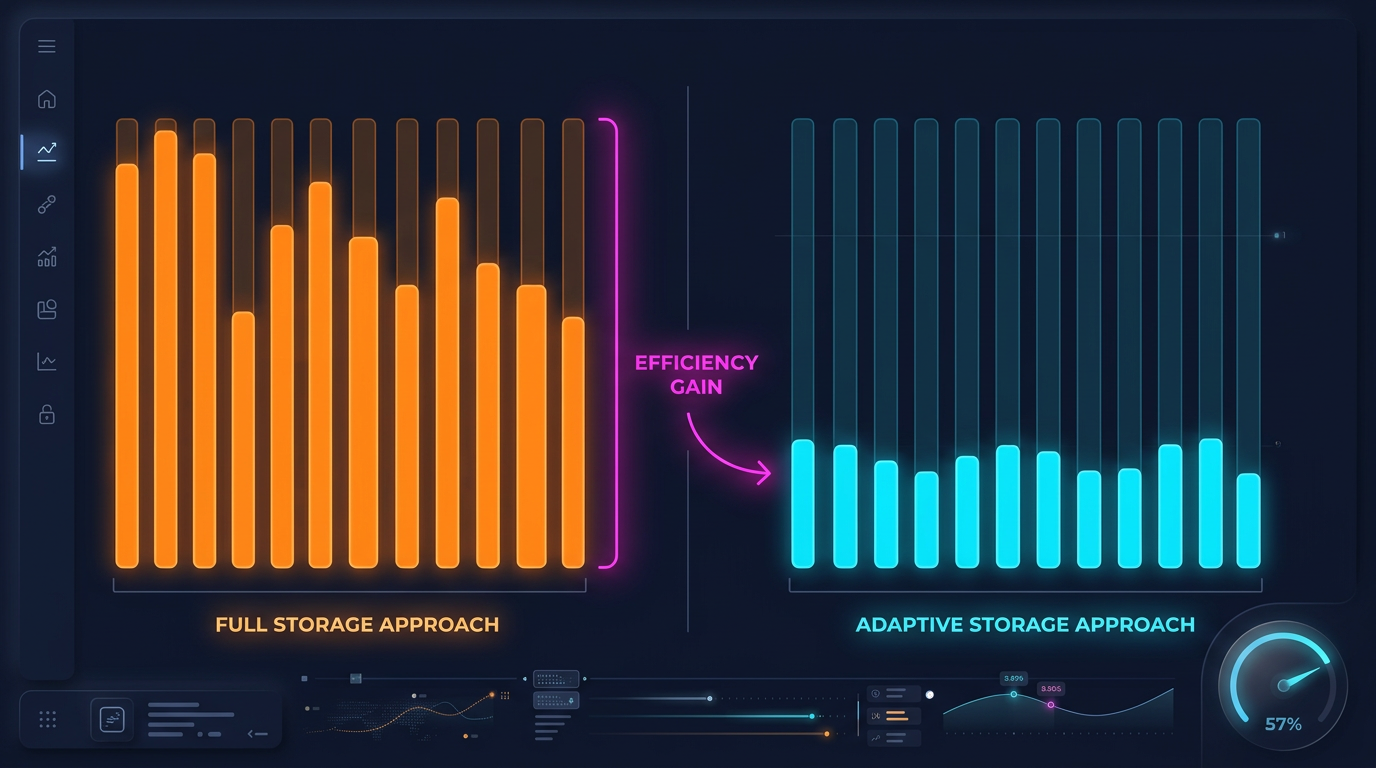

Adaptive Data Storage

Drill-down requires second and millisecond data. But storing everything at maximum granularity is impractical:

Granularity

Bars over 2 years

Parquet size

1m

~1.05M

~15 MB

1s

~63M

~550 MB/month

100ms

~630M

~5 GB/month

A complete 1s archive over 2 years is about 13 GB. 100ms — over 100 GB. Storing everything is possible but wasteful, considering that drill-down uses less than 1% of this data.

Hot-Second Detection

The key observation: seconds in which price moves significantly represent a small fraction. If price changed by less than 0.1% within a second — there's no point storing the 100ms breakdown for that second.

Hot-second detection: when downloading and processing data, we analyze each second and generate 100ms candles only for "hot" seconds — those where price movement exceeded the threshold.

defprocess_trades_adaptive(

trades: pd.DataFrame,

min_price_change_pct: float = 1.0,

) -> tuple[pd.DataFrame, pd.DataFrame]:

"""

Processes raw trades into an adaptive structure:

- 1s candles for all seconds

- 100ms candles only for "hot" seconds

Args:

trades: DataFrame with columns [timestamp, price, quantity]

min_price_change_pct: threshold for drill-down to 100ms

Returns:

(df_1s, df_100ms_hot) — second candles and 100ms for hot seconds

"""

trades['second'] = trades['timestamp'].dt.floor('1s')

df_1s = trades.groupby('second').agg(

open=('price', 'first'),

high=('price', 'max'),

low=('price', 'min'),

close=('price', 'last'),

volume=('quantity', 'sum'),

)

df_1s['price_change_pct'] = (df_1s['high'] - df_1s['low']) / df_1s['open'] * 100

hot_seconds = df_1s[df_1s['price_change_pct'] >= min_price_change_pct].index

hot_trades = trades[trades['second'].isin(hot_seconds)]

hot_trades['bucket_100ms'] = hot_trades['timestamp'].dt.floor('100ms')

df_100ms = hot_trades.groupby('bucket_100ms').agg(

open=('price', 'first'),

high=('price', 'max'),

low=('price', 'min'),

close=('price', 'last'),

volume=('quantity', 'sum'),

)

return df_1s, df_100ms

Storage Savings

For example — ETHUSDT over a typical month:

Approach

Size

Granularity

1m only

~1 MB

1 minute

All 1s

~550 MB

1 second

All 100ms

~5 GB

100 ms

Adaptive

~600 MB

1s + 100ms only for hot seconds

With a threshold of min_price_change_pct = 1.0%, hot seconds account for less than 1% of all seconds. 100ms data for them adds ~50 MB to the 550 MB of second data — a negligible overhead.

If second data is also stored adaptively (only when movement within a minute exceeds 0.1%), the volume can be reduced by another 3-5x.

DELTA_BINARY_PACKED for timestamps: consecutive timestamps differ by a fixed value (60 for 1m, 1 for 1s). Delta encoding compresses them to nearly zero.

BYTE_STREAM_SPLIT for float: splits float32 bytes into streams (all first bytes together, all second bytes together, etc.). For smoothly changing prices, this achieves 2-3x better compression than standard encoding.

ZSTD level 9: good compression with acceptable decompression speed.

float32 instead of float64: sufficient for prices and volumes, saves 50% memory.

Lazy Loading with Caching

Drill-down requests second data for a specific minute. Loading a parquet file for each request is slow. The solution — lazy loading with an LRU cache by month.

from functools import lru_cache

import pyarrow.parquet as pq

import pandas as pd

classAdaptiveDataLoader:

"""

Lazy loader with cache: loads second data by month,

keeps the last N months in memory.

"""def__init__(self, symbol: str, data_dir: str = "data", cache_months: int = 2):

self.symbol = symbol

self.data_dir = data_dir

self.cache_months = cache_months

self._cache_1s: dict[str, pd.DataFrame] = {}

defload_1s_for_minute(self, minute_ts: pd.Timestamp) -> pd.DataFrame | None:

"""Load 1s data for a specific minute."""

month_key = minute_ts.strftime("%Y-%m")

if month_key notinself._cache_1s:

self._load_month_1s(month_key)

if month_key notinself._cache_1s:

returnNone

df = self._cache_1s[month_key]

minute_start = minute_ts.floor('1min')

minute_end = minute_start + pd.Timedelta(minutes=1)

return df[(df.index >= minute_start) & (df.index < minute_end)]

defload_100ms_for_second(self, second_ts: pd.Timestamp) -> pd.DataFrame | None:

"""Load 100ms data for a hot second."""

month_key = second_ts.strftime("%Y-%m")

path = f"{self.data_dir}/{self.symbol}/klines_100ms_hot/{month_key}.parquet"try:

df = pd.read_parquet(path)

second_start = second_ts.floor('1s')

second_end = second_start + pd.Timedelta(seconds=1)

return df[(df.index >= second_start) & (df.index < second_end)]

except FileNotFoundError:

returnNonedef_load_month_1s(self, month_key: str):

"""Load a month of 1s data, evict old data from cache."""

path = f"{self.data_dir}/{self.symbol}/klines_1s/{month_key}.parquet"try:

df = pd.read_parquet(path)

df.index = pd.to_datetime(df['timestamp'], unit='s')

iflen(self._cache_1s) >= self.cache_months:

oldest = min(self._cache_1s.keys())

delself._cache_1s[oldest]

self._cache_1s[month_key] = df

except FileNotFoundError:

pass

Applying Drill-Down to Backtesting

Integration into the backtest loop:

defbacktest_with_adaptive_fill(

states: pd.DataFrame,

strategy_params: dict,

data_loader: AdaptiveDataLoader,

) -> list:

"""

Backtest with adaptive drill-down for fill simulation.

"""

fill_sim = AdaptiveFillSimulator(data_loader)

trades = []

position = Nonefor i inrange(len(states)):

row = states.iloc[i]

ts = states.index[i]

candle_1m = {

'open': row['open'], 'high': row['high'],

'low': row['low'], 'close': row['close'],

'timestamp': ts,

}

if position isnotNone:

fill = fill_sim.check_fill(

ts, candle_1m,

position['sl'], position['tp'],

position['side'],

)

if fill isnotNone:

fill_type, fill_price = fill

trades.append({

'entry_time': position['entry_time'],

'exit_time': ts,

'side': position['side'],

'entry_price': position['entry_price'],

'exit_price': fill_price,

'exit_type': fill_type,

'drill_down': fill_sim.last_drill_depth, # 0, 1, or 2

})

position = Nonecontinue

signal = check_entry_signal(row, strategy_params)

if signal and position isNone:

position = {

'side': signal['side'],

'entry_price': row['close'],

'entry_time': ts,

'sl': signal['sl'],

'tp': signal['tp'],

}

return trades

Both approaches eliminate errors invisible at the daily candle level but critical for realistic backtesting.

Summary: Fill Simulation Approach Comparison

Approach

Accuracy

Speed

Storage

OHLC heuristic (optimist/pessimist)

Low

Instant

1m only

Full 1s backtest

High

Slow (x60)

~550 MB/month

Full 100ms backtest

Maximum

Very slow (x600)

~5 GB/month

Adaptive drill-down

High

~Instant

1m + 1s + 100ms hot

Drill-down provides the accuracy of a full 1s backtest at the speed of a 1m backtest. The key observation: high granularity is not needed everywhere — only at decision points.

Conclusion

Adaptive drill-down is the application of a simple principle: spend computational resources and storage proportionally to data importance.

Three granularity levels:

1m — base pass for 95% of bars

1s — drill-down during fill ambiguity

100ms — drill-down for hot seconds with extreme movement

Three storage levels:

All 1m — complete archive, ~15 MB for 2 years

All 1s — complete or adaptive archive, ~550 MB/month

Hot 100ms only — <1% of seconds, ~50 MB/month

The result: a backtest with tick simulator accuracy at minute-level speed. And storage that grows linearly, not exponentially, with increasing granularity.

@article{soloviov2026adaptivedrilldown,

author = {Soloviov, Eugen},

title = {Adaptive Drill-Down: Backtest with Variable Granularity from Minutes to Milliseconds},

year = {2026},

url = {https://marketmaker.cc/ru/blog/post/adaptive-resolution-drill-down-backtest},

description = {How adaptive data granularity speeds up backtests and saves storage: drill-down from 1m to 1s and 100ms only where price moved significantly.}

}